Dealroom data shows that over 2,800 startups have achieved a valuation of $1 billion or more, or an exit, since 2000, across more than 420 cities worldwide. Since 2018, over 100 new unicorns have been minted yearly, except in 2021, when this number spiked to 787 – a rate of more than two unicorns per day. Over half of these unicorns are based in North America and parts of Asia.

Europe has undergone a remarkable transformation in recent years, with the number of unicorns rising significantly. While estimates vary by source — Dealroom counts 606, Atomico's State of European Tech — 358, and PitchBook lists 229 — the numbers point to the increasing influence of unicorns across Europe. Their emergence not only reflects the maturation of the European venture capital ecosystem but also showcases growing infrastructure, deepening talent pools, and heightened entrepreneurial ambition on the continent.

Vestbee has conducted comprehensive research on the evolution and state of European unicorns, exploring the factors behind their success and the financing challenges they encounter. We also covered the most interesting case studies on companies that achieved or exceeded $1 billion in valuation.

The report focuses on the EU-27 countries, along with the UK, Norway, Ukraine, and Switzerland, with a comparison to other world markets. It’s important to note that the reported number of unicorns in Europe varies across sources due to differing methodologies and definitions. In our research, we define unicorns as privately held, VC-backed companies valued at $1 billion or more following any equity funding round before IPO or acquisition. We rely on data from Dealroom, PitchBook, and reports from Vestbee and European VCs.

Additionally, the report includes a separate special section dedicated to the Central and Eastern Europe (CEE) region, highlighting its unique market dynamics, emerging unicorns, and growth opportunities within this rapidly evolving ecosystem.

The current state of Europe’s unicorn landscape

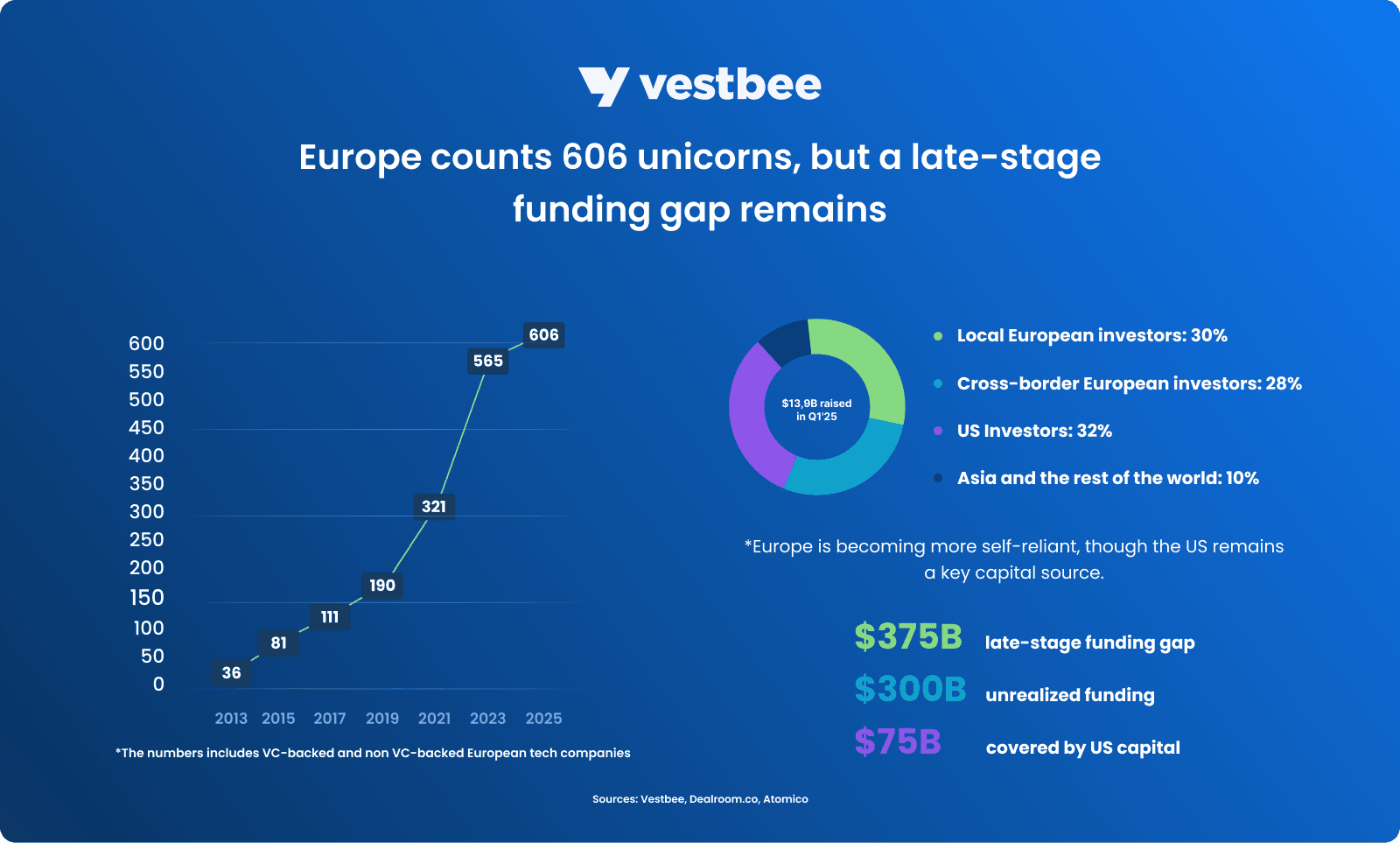

As of Q1 2025, the whole Europe has produced a cumulative total of 606 unicorns, with six new entrants — Neko Health, Tines, Dren Bio, Loft Orbital, Namirial, and Diagnostyka — reaching billion-dollar valuations through funding rounds or exits, as reported by Dealroom. The trend already seems more favorable than in the past year, 2024, when only 16 unicorns appeared. Investment activity signals a gradual recovery, and an ecosystem is seeing a resurgence in spin-outs from existing unicorns, contributing to a compounding “flywheel” effect.

Moreover, the Dealroom’s recent report highlights sustained growth in late-stage investment, with $3.6 billion raised in mega-rounds exceeding $250 million, accounting for 15% of all capital. In comparison, an additional 17% was directed to rounds between $100 million and $250 million. This increase and a strong sectoral focus on healthtech and AI signal increasingly favorable conditions for emerging startups to scale toward unicorn status on accelerated timelines. Notably, four European countries — the UK, Germany, France, and Spain — each raised over $1 billion in venture capital in Q1 2025.

Industry distribution

Europe’s unicorn landscape reflects global trends, spanning a diverse range of sectors. The three dominant industries by number of unicorns are enterprise software, fintech, and healthtech. Over the past five years, the fastest-growing sectors have included legal tech, fintech, robotics, and energy.

Geography of unicorns

Global distribution of $1B + companies

North America, especially the Bay Area, remains the leading hub for unicorn startups. Over the past decade, Europe’s share has steadily increased and now represents roughly 20-30% of new unicorns globally, with the UK consistently contributing the most within the region. China saw rapid unicorn growth in the mid to late 2010s, but recent data indicates its share has declined due to global economic factors. While Europe still trails the US and China in total unicorn counts, the gap is closing, particularly when compared to the Bay Area, which holds about 40-50% of new unicorns worldwide.

European major hubs

The European single market hasn’t eliminated the fragmentation of 27 national systems, with local factors still influencing startup ecosystems. However, by the end of 2015, 11 ecosystems that hadn’t produced a unicorn now boast one or more, says the latest Atomico report. The UK, Germany, and France have seen the most significant gains, going from limited funding before 2014 to a combined $250 billion in the last decade, with the UK nearing $150 billion.

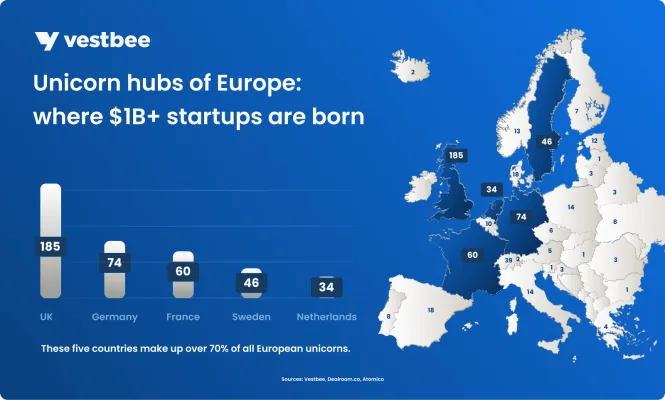

The top 5 countries by the number of unicorn startups collectively account for over 70% of all European $1B+ companies: UK (185 unicorns), Germany (74), France (60), Sweden (46) and Netherlands (34). Regarding the major hubs, capital cities like London, Berlin, Paris, and Stockholm dominate Europe's unicorn scene, with Amsterdam hosting 7% of EU unicorns. In contrast, 68% of US unicorns are in California (about 50%), New York (11%), and Massachusetts (7%), and 62% of China's are in Beijing (30%), Shanghai (20%), and Shenzhen (12%). While Europe’s unicorns are more spread out, key hubs still account for half.

- London remains Europe’s largest unicorn-producing city, thanks to long-established venture capital networks and a big fintech environment. Though Brexit complexities raise cross-border challenges, the UK is still the third country in the world by the unicorn count, as reported by Dealroom.

- Paris has climbed the ranks, with sustained government initiatives (e.g., Bpifrance) helping entrepreneurs in AI, deeptech, and e-commerce.

- Berlin is Europe’s “creative tech capital,” merging lower costs and strong talent pipelines for software-driven businesses. Germany ranks sixth in the world in terms of unicorn count.

- Stockholm and the broader Nordic region have one of the highest unicorn densities in the world, driven by robust digital infrastructure and a strong cultural embrace of entrepreneurship.

- Lisbon, Barcelona, and the wider Southern Europe region are also gaining increasing attention, thanks partly to the rise of remote work, attractive visa programs, and specialized accelerator initiatives.

CEE unicorns

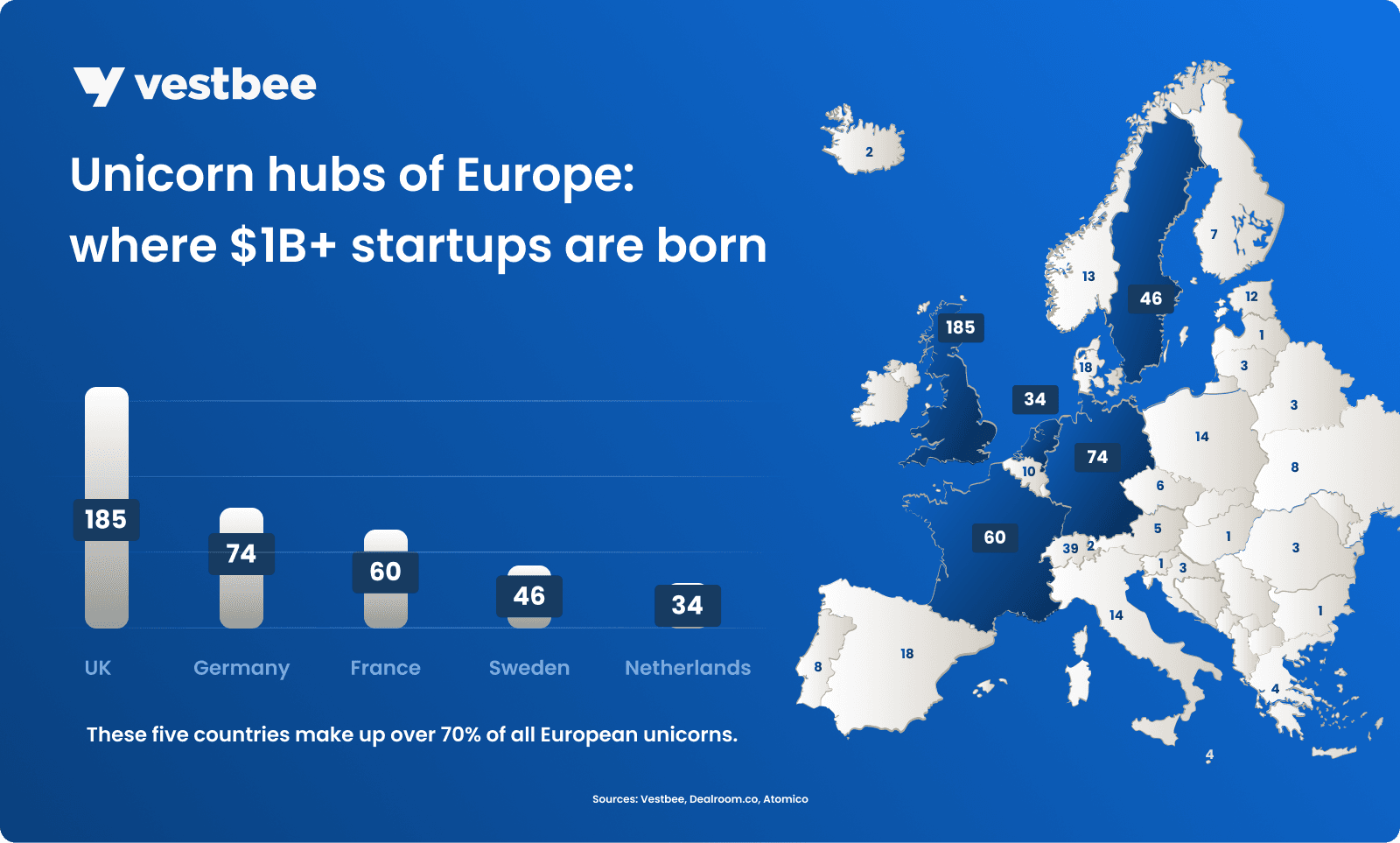

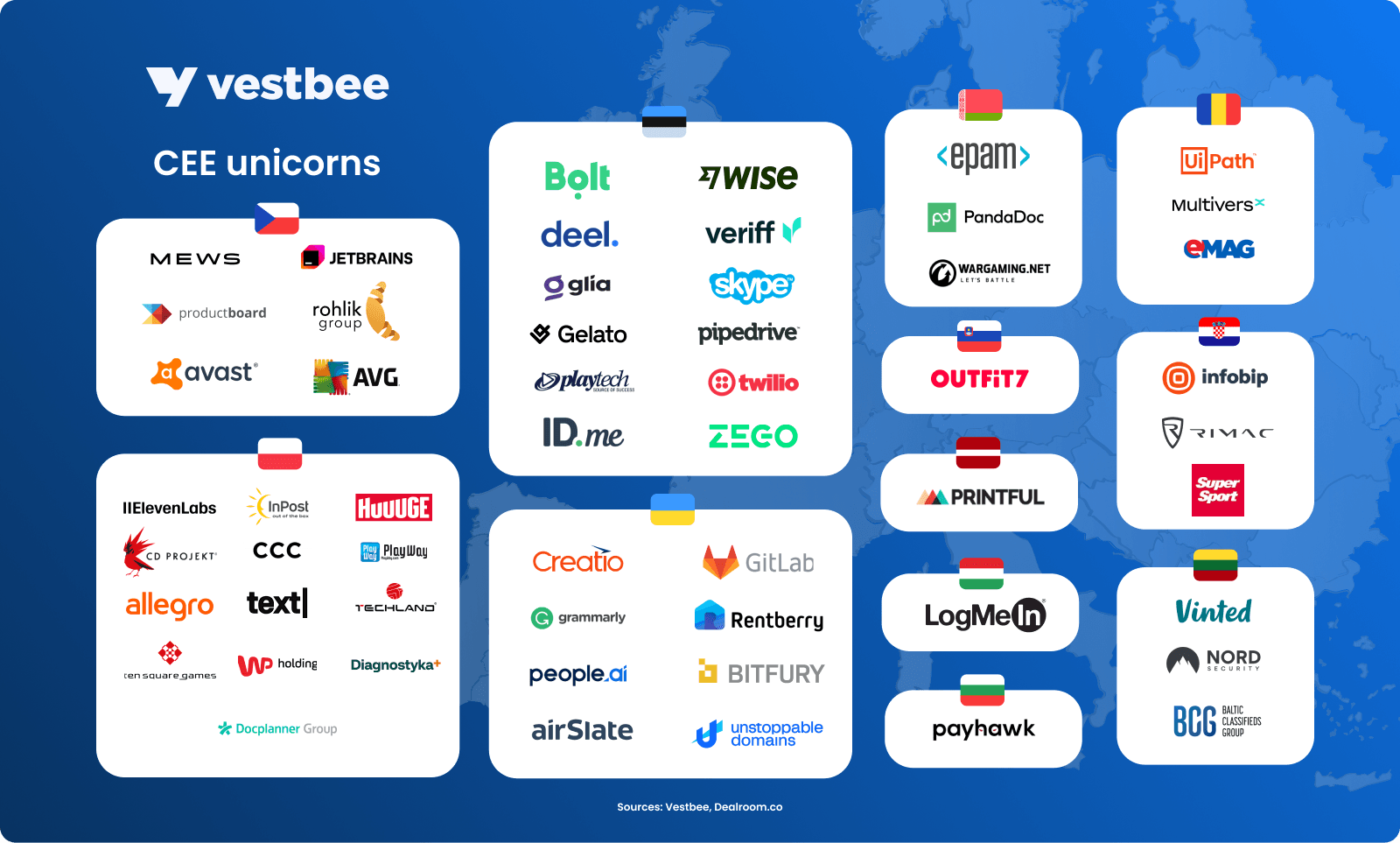

The CEE region has a very special place in the European ecosystem, as even though it trails behind Western Europe in absolute terms, it has produced 56 unicorns with far less capital and involvement from international investors. Between 2015 and 2025, the total value of the CEE startup ecosystem increased by 15.5x, significantly outpacing the European average growth of 7x during the same period. Thus, as of Q1 2025, the total combined enterprise value of CEE startups stands at €243 billion. Poland leads in cumulative ecosystem value at €58 billion, followed by Estonia (€39 billion), Ukraine (€30 billion), and Romania (€28 billion). Lithuania has been the fastest-growing ecosystem since 2020.

CEE unicorns, which we define as either a company with its official headquarters in the CEE region or a company founded by CEE-origin founders that maintains key R&D operations within CEE, are often valued lower than their Western counterparts, despite having comparable revenue or market reach. Notably, around 21% were bootstrapped, starkly contrasting the European average of just 5%. CEE startups typically reach unicorn status with smaller funding rounds, with median values of €8.5 million (Series A), €10 million (Series B), and €31 million (Series C+). In comparison, the European averages stand at approximately €9.6 million (Series A), €22.7 million (Series B), and €36.4 million (Series C+). Despite raising less capital, CEE startups demonstrate higher valuation-to-capital ratios, indicating they create more value per euro invested than the broader European ecosystem.

Estonia leads the region in unicorns per capita, accounting for 18% of all CEE unicorns despite representing only 0.8% of the region’s population. In absolute terms, Poland ranks first with 14 unicorns, followed by Estonia (12), Ukraine (8), and Czechia (6). Moreover, Estonia is the regional leader in breakout capital, while Czechia (e.g., Rohlik, Mews) and Ukraine (Creatio) have secured the most late-stage funding since 2024. A strong “flywheel” dynamic is also emerging in the region, as alumni of unicorn companies increasingly establish their startups. The region also has a robust scaleup pipeline, with over 275 breakout and late-stage companies (those having raised €15 million or more).

CASE STUDY: Creatio

- Founded: 2013

- Valuation as of June 2024: $1.2 billion

- Total funding: $220 million

- Why is it interesting: As one of the few unicorns with Ukrainian roots, Creatio stands out in the CEE region for securing major capital to scale its global no-code CRM platform. The $200 million funding round, led by Sapphire Ventures, underscores investor confidence in enterprise automation and Ukraine’s growing role in late-stage tech investment. Specializing in no-code CRM and workflow automation, the company operates in Boston, London, and Warsaw, serving thousands of enterprise clients worldwide.

Top sectors driving unicorn emergence in the CEE:

- Enterprise SaaS (e.g., Creatio, Productboard, Mews)

- AI and data platforms (e.g., ElevenLabs)

- Healthtech solutions (e.g., Docplanner)

- Mobility, Energy & Climate (e.g., Rohlik, Rimac, Skeleton Technologies)

- Fintech infrastructure (e.g., Payhawk, FintechOS, Symmetrical.ai)

How did Europe’s unicorns evolve

Skype, Spotify, and Klarna: the rise of European unicorns in the 2000s

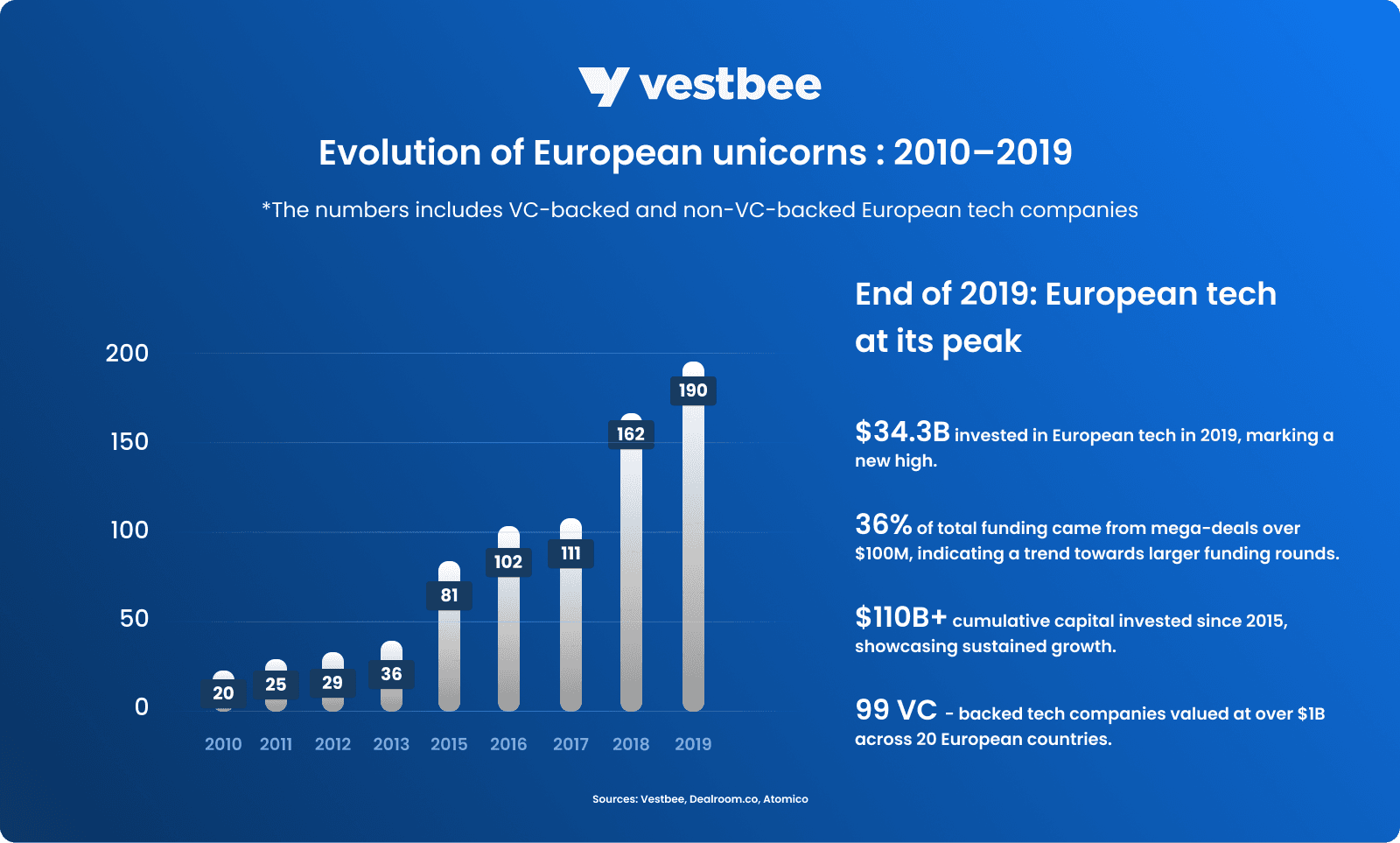

European unicorns have evolved alongside a dynamic venture capital funding and regulatory support shift over the past two decades. Between the early 2000s and mid-2010s, Europe’s venture and startup activity was often fragmented across many national markets, each with its own regulatory approach and funding sources. However, companies like Luxembourg-headquartered Skype, Swedish Spotify, and Klarna proved that global success wasn’t exclusive to Silicon Valley. According to Atomico’s State of Tech report, in 2010, there were 12 unicorns in Europe, and by 2013, the number had more than doubled to 28.

- The Nordics took an early lead with Skype, founded in 2003 by Janus Friis from Denmark and Niklas Zennström from Sweden. Although Skype was incorporated in Luxembourg, its success was deeply rooted in the contributions of a strong IT team from Estonia. The company’s $2.6 billion acquisition by eBay in 2005 highlighted the Nordic region’s innovative potential and sparked the startup boom in Estonia, proving that groundbreaking European tech could thrive beyond the continent’s largest economies.

- Sweden’s following breakouts. By the late 2000s, Sweden became a hub for consumer tech and fintech, fueled by strong digital infrastructure and a risk-taking culture. Klarna (2005) and Spotify (2006) showcased how small, innovative teams could capture global market share and reach $1 billion valuations.

The rise of unicorns in the Nordics in the early 2000s was driven by visionary investors spotting groundbreaking innovations. In 2003, Staffan Helgesson founded Creandum, which led Spotify’s first venture round in 2008. Over the past 20 years, one in every six Creandum investments has become a unicorn, including Klarna, Trade Republic, and Bolt. Helgesson shared insights into Creandum’s approach with Vestbee. Read the interview here.

However, these early success stories remained exceptions rather than the rule. Many first-generation European founders struggled with fewer local VCs, minimal cross-border alliances, and relatively cautious investor mindsets back then. Early unicorn successes often benefited from US or global backers stepping in once the startups gained traction and needed more financial and advisory support.

The 2010s-2019: institutional investors entered the game

In the mid-2010s, European institutional investors, including the European Investment Bank (EIB) and European Investment Fund (EIF), significantly increased their support for high-growth ventures. They co-invested with private funds and addressed early-stage financing gaps. Meanwhile, the EU launched programs like Horizon 2020 in 2014, investing nearly €80 billion into research and innovation over seven years.

Horizon 2020 and related initiatives such as the European Institute of Innovation and Technology (EIT) were crucial in accelerating deeptech and biotech startups. Between 2014 and 2020, EIT invested €2.4 billion, helping launch over 440 startups and supporting nearly 4,000 companies. These efforts helped bring more than 1,500 new or improved products and services to market, attracting €3.9 billion in external investments. Several supported companies achieved unicorn status, including notable names like Verkor, Sword Health, Freyr, Owkin, Ÿnsect, and Climeworks.

As the environment became more favourable for scaling, a significant surge in unicorn formation emerged from 2015 onward. Some of the key factors that enabled this include:

- Maturing VC environment. More substantial seed and growth funds were launched or expanded in Europe, including homegrown VCs such as Balderton, Atomico, and Index Ventures. US funds increased their presence in Europe, investing alongside.

- Improved policy frameworks. Though still in progress, the EU’s push for a Digital Single Market encouraged cross-border expansions. Government-backed accelerators and introducing more startup visas also played a crucial role.

- Cultural shifts. During these years, European founders gradually embraced fast scalability as a valuable and desirable goal.

Since 2015, with the emergence of mega-funds like TCV and Insight Partners closing multi-billion-dollar vehicles (culminating in SoftBank’s $100 billion Vision Fund in 2017), startups with early traction have secured repeated nine-figure rounds, cutting the typical seed-to-unicorn journey from about eight years to just five or six.

CASE STUDY: UiPath

- Founded: 2005

- Total funding: $2B

- Market cap as of April 2025: $6.5B

- Why is it interesting: launched in Romania and relocated to the US, UiPath became a global enterprise software leader. After a $1.6M seed round in 2015, it raised $30M in Series A (2017) and $153M in Series B (2018), reaching unicorn status just three years after its seed. UiPath’s rise shows how early traction and mega-fund access can fast-track growth, even from undercapitalized ecosystems.

2016 to 2018 marked a transition from foundational growth to acceleration and sectoral diversification within the European unicorn landscape. This period was defined by the continued dominance of consumer-facing platforms and the rise of early fintech leaders such as TransferWise (now Wise), Revolut, and N26. These companies capitalized on growing digital-native user bases and increasingly streamlined regulatory frameworks for digital financial services, particularly in the UK, which emerged as Europe’s most prolific unicorn hub.

CASE STUDY: N26

- Founded: 2013

- Total funding: $1.7B

- Valuation as of April 2023: $6B

- Why is it interesting: N26 was the first company to reach unicorn status in 2019, securing a $300 million round in January. It had a rapid ascent to unicorn status within a few years, disrupting traditional banking with its fully digital model. Despite operating in a highly regulated sector, it gained significant market traction and investor confidence. Its successful international expansion, including into the US, highlights its growth.

By the end of 2017, Europe had produced a cumulative total of 41 unicorns, seven of which joined the list that year. Momentum continued into 2018, which saw a sharp year-over-year increase in the total number of unicorns. The cumulative number rose to 61 by year-end — a 49% increase from the previous year. Moreover, 12 of these 61 companies had surpassed the $5 billion valuation mark, with five advancing into decacorn territory (valued at $10 billion or more). The increasing density of developer talent, combined with more readily available growth capital, generated a flywheel effect in leading ecosystems. By 2019, Europe entered a new phase marked by rapid scale, increased velocity of unicorn creation, and more profound structural diversification across regions and sectors.

2020 pandemic-led growth

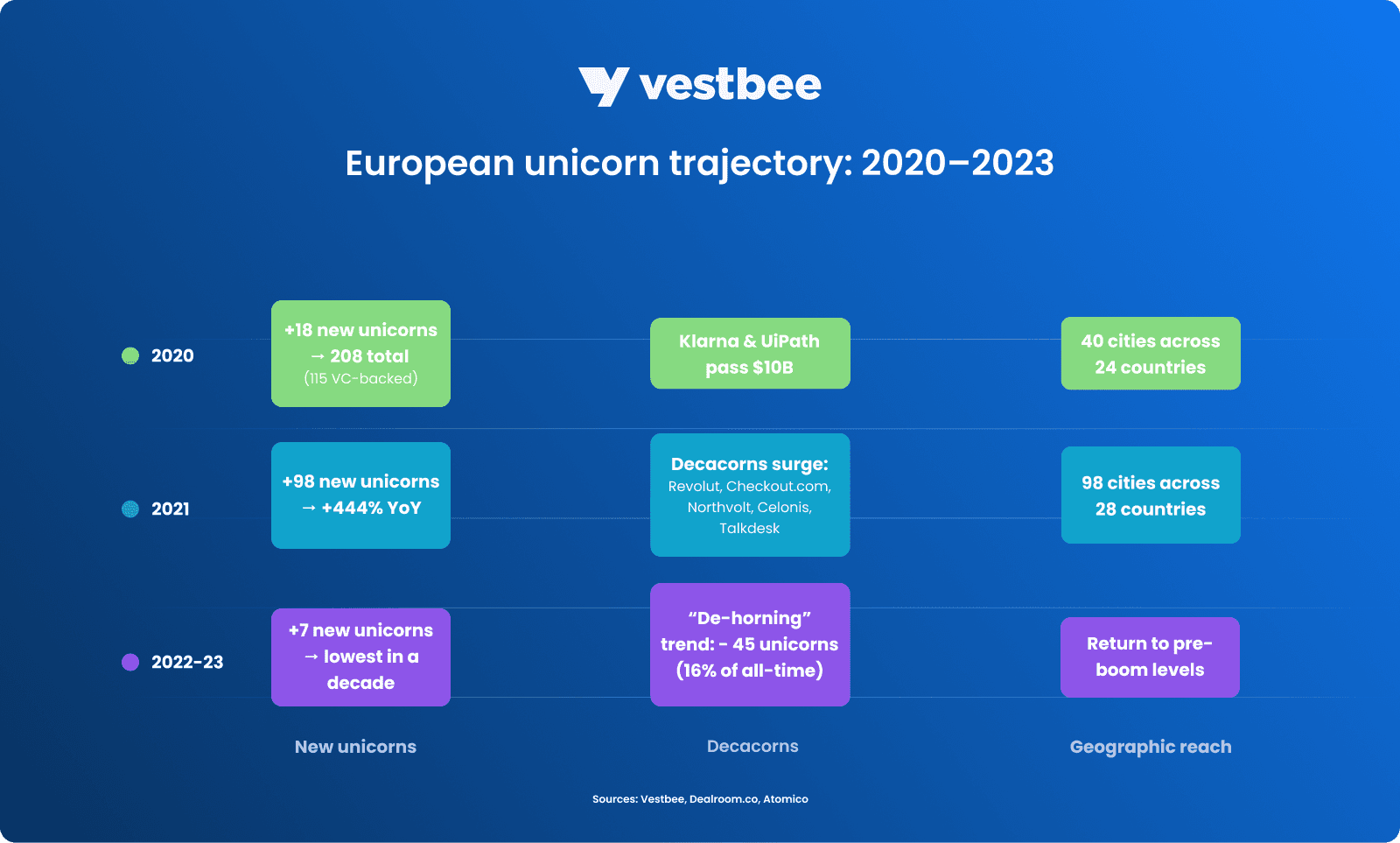

Despite pandemic-driven uncertainty, 2020 marked a breakthrough year for European tech. The continent added 18 new unicorns, reaching 208, including 115 VC-backed. More than the numbers, 2020 stood out for the speed of scale, the emergence of decacorns, and the widening geographic footprint.

- Speed of scaling: previous speed records were shattered. Cazoo hit unicorn status in 18 months; Hopin surpassed it by reaching $2.1B in 17 months, becoming Europe’s fastest unicorn (Covid unicorn Hopin was formally marked “defunct” in 2024, with RingCentral as its successor).

- First decacorns: Klarna and UiPath became Europe’s first VC-backed decacorns, surpassing $10B in valuation.

- Geographic expansion: at least 40 cities in 24 countries had produced a unicorn by year-end. While hubs like London and Stockholm remained central, cities like Tallinn and Cluj-Napoca gained ground. Key unicorns included Arrival, Bolt, Hopin, Lilium, MessageBird, and Pipedrive.

- Sector trends: beyond fintech and enterprise software, strong activity emerged in transportation tech (Cazoo secured a $310 million Series D), cybersecurity (Snyk and MessageBird each closed rounds of $200 million), and healthtech (Ÿnsect and InnovaFeed attracted $372 million and $165 million respectively) — a notable shift toward impact-driven ventures aligned with UN SDGs on climate, sustainable cities, and health.

- Valuation surge: the combined value of European unicorns hit $1.09 trillion, driven by mega-deals like Northvolt ($600M), Klarna ($650M), UiPath ($225M), and Checkout.com ($150M).

Crucially, geographic distribution broadened: unicorns were now emerging from 98 cities across 28 countries, including Latvia and Cyprus, with Printful and Nexters Group joining the billion-dollar club. The UK solidified its lead as the continent’s startup capital, reaching 100 unicorns.

Valuation corrections and unicorn declines

In the following years, the European unicorn landscape experienced a sharp downturn. Unicorn creation in 2022 returned to a rate more consistent with 2018-2020 averages, showing that the explosive growth of the previous year was more of an outlier than a signal of a new ecosystem formation.

Many of the $1B+ companies that appeared in 2022 were already nearing this status in 2021, and significantly, 45 companies lost their unicorn status that year, accounting for 16% of all former unicorns. This trend highlighted the phenomenon of “paper unicorns” — startups that had reached billion-dollar valuations primarily due to inflated private market investments rather than sustainable business fundamentals. As market volatility increased, these inflated valuations proved difficult to maintain, resulting in widespread devaluations.

In 2023, only seven companies reached unicorn status — the lowest number in the decade, and even more of them were “de-horned”. The primary sectors for new unicorns were AI and machine learning, with successes from AI-driven startups like Mistral AI and Aleph Alpha.

CASE STUDY: Mistral AI

- Founded: 2023

- Valuation as of 2024: $6.2B

- Total funding: €1.1B

- Why is it interesting: Mistral AI is an exceptional unicorn case: it reached a $2 billion valuation just months after launching, without a commercial product, driven purely by its open-source LLMs and Europe's hunger for sovereign AI. Its rapid ascent reflects both investor confidence in elite technical teams and geopolitical urgency around AI independence from US tech giants.

Several key factors fueled this downturn:

- The collapse of late-stage capital availability,

- Ongoing valuation compression,

- Lower participation of international investors.

In this environment, many unicorns became “value-stuck” — unable to IPO, unwilling to accept down rounds, and slow to exit. The focus shifted from growth at all costs to a more balanced emphasis on unit economics and business durability.

Key opportunities and challenges for European unicorns today

Late-stage funding gap and consumer demand

Europe’s scaleups continue to face a deepening growth-stage funding gap, now estimated at $375 billion. Since 2015, limited conversion to later-stage rounds has left $300 billion in unrealized funding on the table. On top of that, European investors increasingly rely on US capital to plug a further $75 billion shortfall, as highlighted in Atomico’s report.

Structural challenges in Europe’s market compound this funding gap. While the US enjoys strong consumer demand, with consumption making up 70% of GDP, and a large, unified market for B2C growth, European startups often hit ceilings earlier. Fragmentation across languages, regulations, and purchasing behavior makes it harder to scale efficiently across borders. As Dealroom notes, many European unicorns are pressured to expand prematurely or defensively, especially as US and Asian players move aggressively into local markets. The result is increased user acquisition costs and a growing strain on already limited growth capital.

CASE STUDY: Hopin

Hopin, a UK-based virtual events platform, experienced meteoric growth during the COVID-19 pandemic. Founded in 2019, it capitalized on the global shift to online events, achieving a valuation of $7.75 billion by 2021 after raising over $1 billion from prominent investors such as Andreessen Horowitz and General Catalyst.

However, as in-person events resumed, demand for virtual platforms waned. In response, Hopin sold its core events business to RingCentral for just $50 million in 2023, starkly contrasting its previous valuation. The company underwent significant restructuring, including layoffs and leadership changes, as it faced challenges sustaining rapid growth post-pandemic. In 2024, Hopin was formally marked “defunct.”

Despite global uncertainty, Dealroom data through Q1 2025 shows a notable shift: local European investors now contribute the largest share of funding to European startups, accounting for 30% of total capital raised. Combined with 28% from cross-border European investors, over half of all funding originates within Europe — a sign of a maturing and increasingly self-reliant venture ecosystem. Still, over 40% of funding comes from overseas, led by the US (32%), underlining Europe’s global connectivity.

Interestingly, while European unicorns typically raise less capital than their US or Chinese counterparts, they rely on a broader investor base (9.9 on average) to reach the $1 billion valuation, reflecting Europe’s collaborative, syndicated funding model. For comparison, US unicorns average 7.3 investors, and Chinese unicorns just 5.3.

CASE STUDY: Northvolt

Northvolt, a Swedish battery manufacturer founded in 2015, aimed to become Europe's leading supplier of lithium-ion batteries for electric vehicles. The company attracted substantial investments, raising over $15 billion from investors like Goldman Sachs and BlackRock.

Despite this, Northvolt faced production delays, supply chain issues, and increasing competition from Chinese manufacturers. These challenges culminated in the company filing for bankruptcy in Sweden in March 2025, marking one of the largest industrial bankruptcies in the country's history.

Talent & entrepreneurial culture

European scaleups often struggle with talent shortages in areas like green tech and digital innovation. Yet with 6.1 million developers, the region has a strong base for growing tech ecosystems. Cities like Berlin, Stockholm, and Lisbon are emerging as magnets for talent, reflecting a shift toward more entrepreneurial, risk-tolerant cultures. However, intense global demand — especially for AI and quantum experts—continues to draw top talent to the US. According to PwC, 64 EU-27 unicorns have relocated to the US, while only 10 have moved into Europe, such as Poolside AI, which shifted from the US to France.

Regulations

Europe’s digital single market has eased some barriers to cross-border growth, but regulatory fragmentation remains a significant challenge for unicorns. Companies must still navigate 27 national systems with differing rules on taxation, labour, data privacy, and IP protection, slowing expansion and raising costs. Alongside the European Investment Bank’s push for greater harmonization in areas like IP, tax incentives, and insolvency rules, the European Commission and other entities have also taken steps to reduce friction, foster a more cohesive regulatory environment, and support faster, more scalable growth across the continent.

The majority of deals are concentrated in Western and Northern Europe

Over 65% of current EU unicorns are located in the UK, Germany, or France, with most clustered in capital cities or established entrepreneurial hubs. Startups outside these areas face more challenges scaling quickly, including limited local VC support, fewer cross-border financing options, and a lack of a strong entrepreneurial culture that often drives successful ecosystems.

***

European startups that became unicorns in 2024

Europe welcomed 11 new unicorn companies in 2024, securing a combined approximately €3 billion. The UK and France led with three new unicorns each, followed by the Netherlands, Belgium, Germany, and Italy, each adding one.

- Wayve, UK

Wayve has raised a $1.05 billion Series C investment round led by SoftBank Group, with contributions from new investor NVIDIA and existing investors.

- team.blue, Belgium

team.blue, a Ghent-based digital enabler for SMBs in Europe, has secured a €550 million investment at a €4.8 billion valuation. The capital came from CPP Investments.

- Poolside AI, France

Poolside, a startup developing an AI coding assistant for software engineers, has raised $500 million Series B led by Bain Capital Ventures at a $3 billion valuation.

- Lighthouse, UK

Lighthouse, a firm building AI-powered hotel software, has raised a $370 million Series C round, led by KKR. The recent round pushed the startup to unicorn status.

- Flo Health, UK

Femtech startup Flo Health, which develops an app to help people track menstrual cycles, raised a $200 million-plus Series C from General Atlantic at a $1 billion-plus valuation.

- EGYM, Germany

EGYM has raised approximately $200 million of growth capital at a valuation of over $1 billion from L Catterton, a leading global consumer-focused investment firm.

- Bending Spoons, Italy

Italian app developer Bending Spoons has raised $155 million through its latest capital increase, taking the company's valuation to $2.5 billion.

- Newcleo, France

Newcleo, a clean nuclear technology company, has closed a Series A capital raise, securing €135 million, and relocated its HQ to Paris.

- Pigment, France

Business forecasting platform Pigment has raised €133 million in Series D funding led by ICONIQ Growth, Sandberg Bernthal Venture Partners.

- DataSnipper, the Netherlands

DataSnipper, has secured $100 million in a Series B funding round led by Index Ventures, at a valuation of $1 billion.

- Pennylane, France

Accounting platform Pennylane has raised a €40 million Series C round, bringing its valuation to €1 billion. DST Global led the funding.

CEE startups that became unicorns in 2024

- Creatio, Ukraine / the US

Creatio offers a no-code platform enabling businesses to automate customer relationship management. In June 2024, Creatio raised $200 million in a round led by Sapphire Ventures, achieving a $1.2 billion valuation and securing its status as a unicorn.

- Mews, Czech Republic / the Netherlands

Mews provides a cloud-based property management system designed to automate and simplify hotel operations. In March 2024, Mews raised €100 million in a Series C round led by Kinnevik, reaching a valuation of $1.2 billion and becoming Czechia's 6th unicorn.

- ElevenLabs, Poland / the UK

ElevenLabs specializes in AI-driven text-to-speech and voice cloning technologies, producing lifelike speech synthesis. In January 2024, ElevenLabs raised $80 million in a Series B funding round, which pushed its valuation to $1.1 billion.

- Blueground, Greece

Blueground offers fully furnished, long-term rental apartments in major cities worldwide. In March 2024, Blueground secured €42 million in a Series D funding round, pushing its valuation over $1 billion.

If you have any feedback or thoughts on the report, feel free to drop me a line!