The Central and Eastern European startup ecosystem has a distinctive place on the European innovation map. While it still trails behind Western Europe in the number of scaleups and total funding, its growth trajectory has been defined by strong technical talent, lower operating costs, availability of public funding, and the increasing involvement of both regional and international investors.

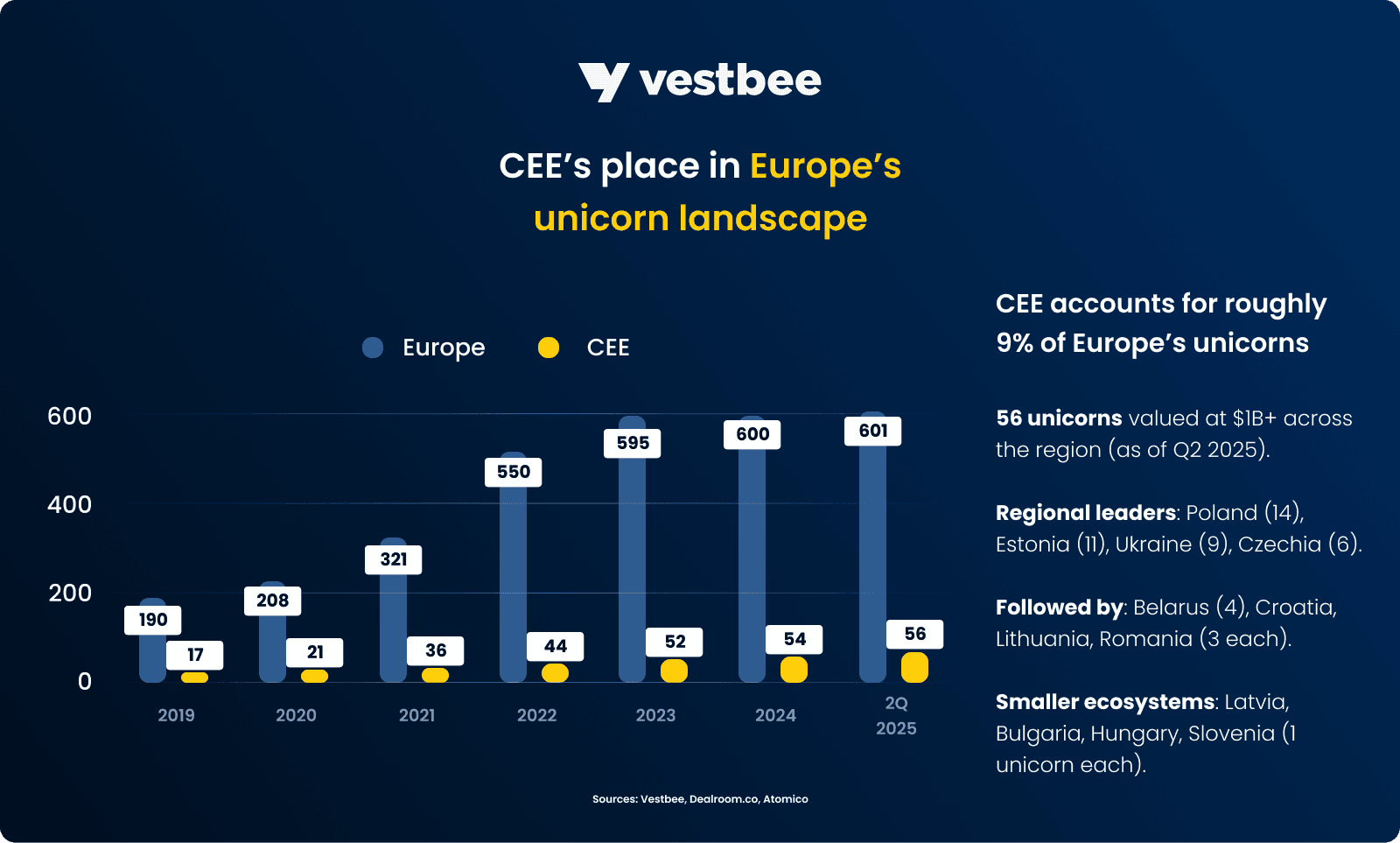

This evolution unfolds alongside a broader shift across Europe’s startup scene, which continues to mature. As of Q1 2025, the continent counts 601 unicorns, with 16 new ones formed in 2024 and 15 so far in 2025. Although the pace has slowed since the boom of 2020–2021, the emphasis on quality over quantity signals a more sustainable and balanced market.

To learn more about Europe’s unicorns, explore Vestbee’s latest report — a comprehensive look at their evolution, success factors, funding challenges, and standout case studies of companies that reached or exceeded $1 billion in valuation.

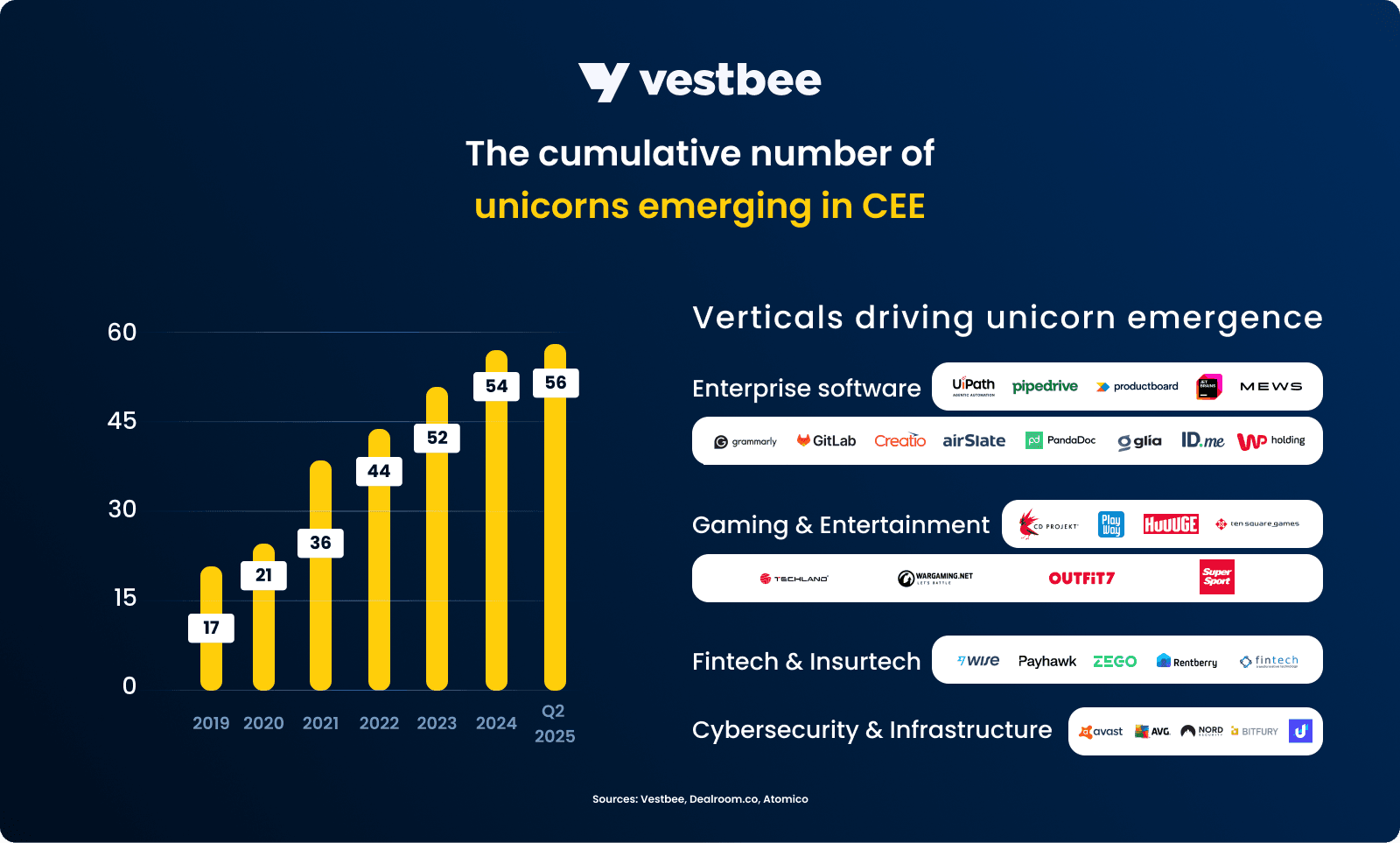

Despite operating with far less capital and limited international investor engagement, the CEE region has already produced 56 unicorns, with five emerging over the last two years. The ability of an ecosystem to consistently build billion-dollar companies remains one of the clearest indicators of its maturity, placing the CEE as one of the key contributors to Europe’s innovation economy.

A word on methodology

This report provides an in-depth overview of the CEE unicorn landscape, focusing on the companies that reached unicorn status between 2024 and 2025. For this analysis, unicorns are defined as privately held venture-backed startups valued at $1 billion or more before IPO or acquisition, following Dealroom’s criteria.

Our primary dataset comes from Dealroom, covering company counts, valuations, and timelines, complemented by additional insights from PitchBook, Crunchbase, and Vestbee’s proprietary market intelligence. To ensure data accuracy and contextual depth, our report also references leading industry publications and regional ecosystem reports.

CEE startup ecosystem overview

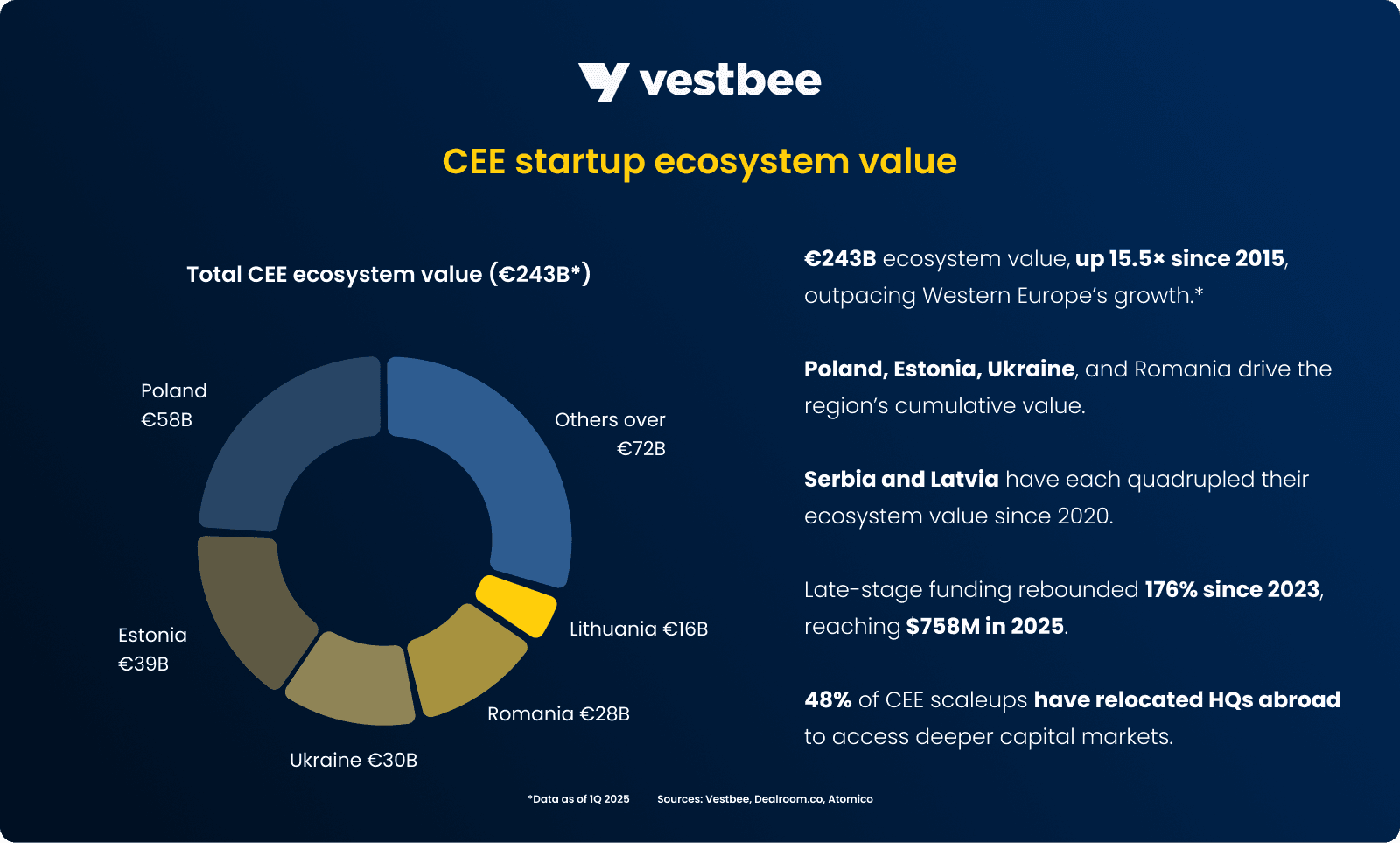

As of the first quarter of 2025, the CEE startup ecosystem has reached a combined enterprise value of €243 billion, a 15.5× increase since 2015 — more than double the growth rate of Western Europe, which expanded 7× over the same period. Poland remains the regional leader with €58 billion in cumulative startup value, followed by Estonia with €39 billion, Ukraine with €30 billion, and Romania with €28 billion. While Lithuania’s ecosystem is smaller at around €16 billion, it has been the fastest-growing since 2020, expanding nearly sixfold in five years. Similar strong growth trajectories have been recorded in Serbia and Latvia, each more than quadrupling its ecosystem value since 2020.

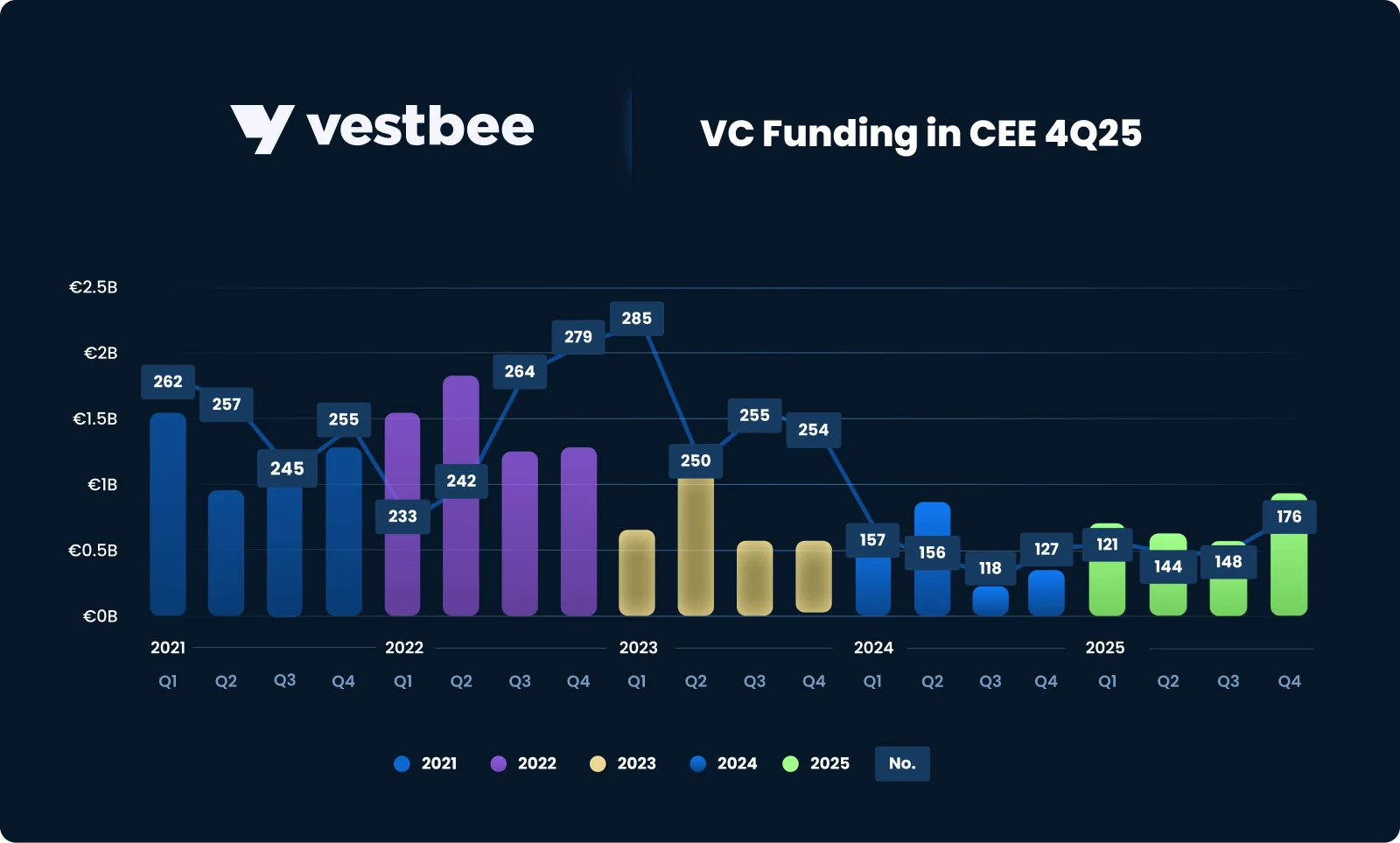

However, in Q1 2025, deal volume in the CEE fell 23% year-over-year, and overall capital deployment contracted despite total funding reaching €700 million. A 9% increase from Q1 2024 was largely driven by ElevenLabs’ €170 million Series C. In the following quarter, CEE startups closed 144 publicly reported rounds, raising over €640 million in total. A few landmark raises, including Cast AI, Aerones, and Pactum, lifted headline figures, yet investor appetite remained cautious. It’s a pattern Vestbee continues to observe in the region — ecosystem growth still depends on occasional blockbuster deals rather than steady investment flows.

This uneven landscape has also influenced where the startups choose to scale from. Nearly half of CEE’s total enterprise value comes from startups that have relocated their headquarters outside CEE, often to gain access to deeper capital markets and international customers. As Dealroom data shows, 48% of CEE scaleups moved their HQ to another country than their country of origin.

Funding dynamics and capital efficiency

When examining the potential of unicorn creation, it’s worth looking at the state of the late-stage funding rounds in the region. Although dedicated growth-stage VCs remain relatively scarce in CEE, between 2020 and 2024, around 74% of all venture capital invested in the region went into breakout (€15-100 million) and late-stage (€100 million+) rounds. In total, it accounted for roughly 250 deals — about 4% of all such rounds in Europe.

Late-stage funding has also rebounded sharply in recent years — it peaked in 2021 with €3.5 billion, collapsed to €275 million in 2023, and then nearly tripled to €818 million in 2024. So far in 2025, the region recorded $758 million in late-stage rounds of $100 million and above — across just 5 transactions.

Notably, the CEE ecosystem has repeatedly shown resilience. During the global VC downturn of 2023, when investments in Western Europe plunged by 35%, funding in CEE contracted by just 15%. The local startups have also proven to be exceptionally efficient in capital utilization — scaleups tend to grow faster and reach the $1 billion mark more often through bootstrapping or lean financing than their Western European peers.

According to Dealroom, around 79% of CEE billion-dollar companies were backed by VC or growth capital at some stage, compared to 95% across Europe. While countries like Bulgaria, Hungary, and Slovenia boast fully VC-backed unicorn portfolios, others, including Poland, with 29% of bootstrapped unicorns, Croatia — 33%, and Romania — 33%, show a stronger presence of self-funded success stories.

Thus, despite limited access to growth capital across the region over the past decade, this efficiency is now creating a flywheel effect: talent and experience gained in high-growth tech firms are being reinvested into the next generation of founders. More than 300 former employees of leading regional unicorns, such as Wise, Bolt, Allegro, EPAM, Veriff, Pipedrive, Rimac, and InPost, have gone on to found or co-found new startups and scaleups. These spinouts include companies like NFTPort, PandaDoc, Klaus, SaltoX, Katana, and Omnipack, spanning both early-stage and more established ventures.

Where CEE unicorns stand in Europe’s unicorn race

Europe’s startup ecosystem continues its measured recovery from a sharp downturn subsequent to the 2021 peak. According to Dealroom, the continent now counts 601 active unicorns, with 16 new additions in 2024 and 15 so far in 2025. Late-stage investment has regained strength, with $3.6 billion raised in mega-rounds exceeding $250 million (around 15% of all VC capital), driven largely by healthtech and AI scaleups. The four heavyweight markets: the UK, Germany, France, and Spain, each attracted over $1 billion in venture funding in Q1 2025.

Within this landscape, CEE accounts for roughly 9% of Europe’s unicorns, with 56 companies reaching the $1 billion valuation mark. The roster is led by Poland (14), Estonia (11), Ukraine (9), and Czechia (6), followed by Belarus (4) and Croatia, Lithuania, and Romania (3 each). Smaller ecosystems, including Latvia, Bulgaria, Hungary, and Slovenia, have each produced at least one billion-dollar company.

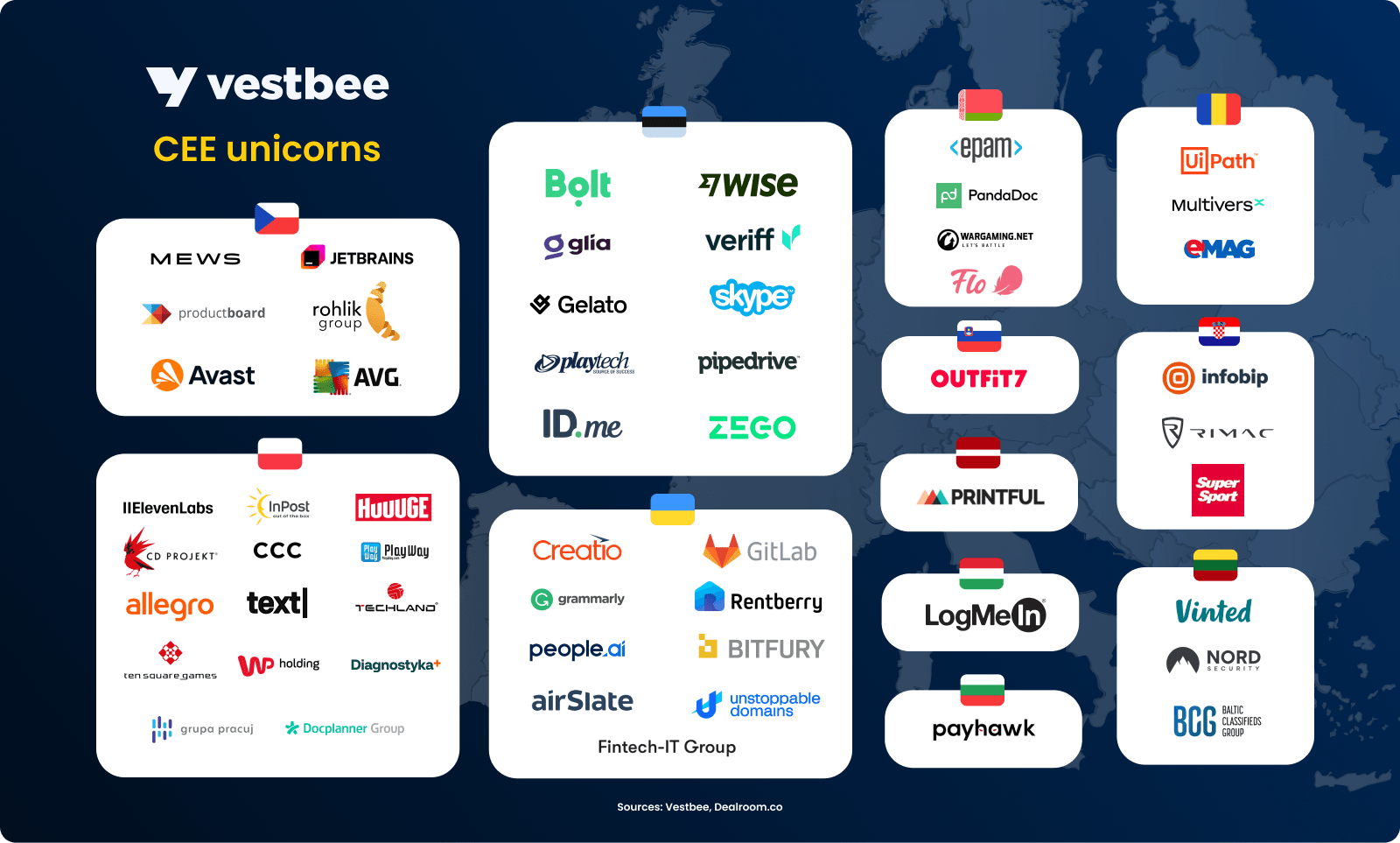

Among the region’s most valuable unicorns are Grammarly (Ukraine-founded, $13 billion), Wise (Estonia-founded ($13 billion), Allegro (Poland-founded ($9.4 billion), and ElevenLabs ($6.6 billion). In terms of total funding raised, UiPath (Romania-founded, $2.0 billion), Bolt (Estonia-founded, $1.9 billion), Rohlik (Czech-founded, $763 million), and Rimac Automobili (Croatia-founded, $759 million) top the charts.

The trajectory of unicorn creation in CEE initially showed dynamic growth before entering a more sustainable phase. The number of billion-dollar companies climbed from 17 in 2019 to 55 by the end of 2024, with 2021 marking the peak year — 15 new unicorns, or a quarter of all ever created in the region. Growth remained steady in 2022 and 2023 (8 new unicorns each year), before slowing in 2024-2025 as valuations adjusted and funding cycles normalized.

What stands out, however, is how CEE-born unicorns increasingly combine local roots with global reach. Many successful startups retain core R&D or engineering teams in the region while expanding commercially from major hubs like London or New York. This combination of local R&D and global expansion shows a clear pattern: while many CEE-born unicorns scale from international markets, their core innovation still comes from regional tech hubs, which raises the question of where exactly they are built.

Geography of CEE unicorns

Most of CEE’s unicorn growth between 2024 and 2025 comes from Poland, Estonia, and the Czech Republic, with Ukraine and Romania following closely. Unlike Western Europe, where activity is concentrated in a few major cities like London, Berlin, and Paris, CEE’s billion-dollar companies are spread across a network of national hubs — a distributed model that has become one of the region’s key advantages.

Leading hubs and their strength

Poland is CEE’s largest market, with a startup ecosystem valued at around €58 billion, which leads in unicorn count — 18 companies, according to the latest data from Dealroom’s report, co-authored by Vestbee, SHAPE Capital Partners, and Cogito Capital Partners. Warsaw, home to companies like Booksy and DocPlanner, and Krakow, with headquarters of InPost, serve as the country’s primary hubs.

Estonia is the CEE’s per-capita champion, with an ecosystem valuation of €39 billion. With just 1.3 million people, it has produced 14 unicorns, giving it the highest unicorn density in the world. The World Economic Forum credits this performance to the country’s digital-first policies and the “flywheel effect”, where founders from early successes like Skype launch new ventures.

Estonia represents 18% of CEE’s unicorns while accounting for only 0.8% of the region’s population. With standout companies like Bolt and Pipedrive, Tallinn has emerged as the country's leading tech hub.

Emerging CEE ecosystems

Beyond these leaders, other CEE countries are steadily building their own strong ecosystems:

- Ukraine, despite the war, maintains a tech sector valued at €30 billion with nine unicorns. Its most recent billion-dollar company is Fintech-IT Group, a developer of a popular neobank mono.

- The Czech Republic, with its engineering tradition and industrial base, is a late-stage funding leader, which hosts six unicorns, including Rohlik and Mews. Its ecosystem is valued at €25 billion.

Lithuania and Romania are emerging as high-potential ecosystems, each currently hosting three unicorns. Lithuania has been CEE’s fastest-growing ecosystem since 2020, with an ecosystem valuation of €16 billion, while Romania already has an ecosystem valuation of €13 billion and continues to expand its pool of tech ventures.

Scaleup landscape and the paradox of scaling

The CEE scaleup ecosystem is highly geographically diverse, with different countries playing complementary roles across various stages of growth. For this report, we adopt Dealroom’s definition of scaleups as companies in the breakout, late-stage, or unicorn phase.

Poland leads in the number of scaleups, hosting 60 firms, followed by Estonia with 54, the Czech Republic with 38, Ukraine with 26, and Romania with 21. Funding patterns further underscore each country’s specialization: Poland dominates early-stage capital, raising €167 million since 2024; Estonia excels in breakout-stage funding, raising €312 million; while the Czech Republic and Ukraine lead in late-stage investment, securing €255 million and €182 million, respectively.

Overall, CEE is one of the fastest-growing startup hubs, with over 270 scaleups, outpacing Europe’s growth over the past decade. Yet, the region faces a paradox: scaling still remains challenging, because late-stage funding is scarce. That is why relocation has become a natural step for many CEE scaleups — 48% of them have been relocated abroad, with Ukrainian companies having the highest relocation rate.

With local markets often too small to sustain global ambitions, companies relocate their headquarters to the West to access larger, more mature markets. In number, 56% of scaleups moved to the US, 39% — to other European countries, including 24% to the UK. Beyond the benefit of being connected to the global ecosystem, CEE companies often relocate for reasons such as:

- Better visibility to global investors

- Legal, tax, or regulatory frameworks aligned with international capital

- Brand and recruitment advantages. It is easier to persuade global talent if the startup is “headquartered” in a major Western jurisdiction

Given these factors, relocation is often seen by investors as a logical and even encouraging next step. As Dan Lupu, Venture Partner at Earlybird, told Vestbee: “In Eastern Europe, local markets are too small to build unicorns, so companies must step out of their comfort zones and build products with a broader reach. Relocated startups usually still have development teams and other resources across CEE, but if you want go-to-market or marketing resources, which are fairly scarce in CEE, you need them closer to your clients”.

Sectoral landscape of unicorns

In terms of sectors, enterprise software, AI, and fintech dominate the CEE scaleup and unicorn landscape, with a total of 237 companies in these fields. These sectors represent not only CEE’s strongest comparative advantage — deep engineering talent and cost-efficient R&D, but also align closely with global technology investment trends.

Leading verticals

When measured by startup activity, the CEE startup landscape remains highly concentrated around enterprise software, AI, and fintech.

Enterprise software, particularly SaaS, continues to be the region's primary growth engine, hosting the largest number of companies across early and growth stages — almost 800, according to Dealroom. The sector strength is reflected in the success of CEE-born players like Pipedrive and Grammarly, which shows how B2B solutions from the region can scale from smaller markets to global reach.

Artificial intelligence has become the second-largest and one of the fastest-growing verticals, with over 650 startups, fueled by the region’s deeptech capabilities and strong academic tradition in computer science and engineering — particularly across Poland, the Czech Republic, and Ukraine. Fintech follows, supported by CEE’s expertise in financial engineering, with billion-dollar firms like Fintech-IT Group and Payhawk strengthening the region’s global competitiveness.

Beyond these dominant verticals, deeptech, martech, transportation, health and climate tech, energy, and security also rank among the CEE’s most popular sectors. Although these industries are smaller in number compared to the top three, they are growing fast — and this is evident in the increasing amounts of capital they raise.

Funding by sectors

Thus, the funding landscape no longer mirrors the distribution by startup count. In 2024, transportation, fintech, and energy led in total capital raised — €436.7 million, €378.5 million, and €343.7 million, respectively. Enterprise software with €293.2 million, health — with €284.3 million, and marketing — €246.5 million, followed closely behind.

By 2025, funding flows have shifted. Fintech emerged as the top-funded sector with $633 million raised, followed by enterprise software with $607 million and security with $449 million, reflecting a broader transition toward financial technology and digital resilience as the key investment themes of the region.

Zooming in on unicorns, here are the sectors driving their rise in CEE:

- Enterprise software, with UiPath, Pipedrive, Productboard, JetBrains, Mews, Grammarly, GitLab, Creatio, airSlate, PandaDoc, Glia, ID.me, and WP Holding, operating across it.

- Gaming & Entertainment: CD Projekt, PlayWay, Huuuge Games, Ten Square Games, Techland, Wargaming, Outfit7, and SuperSport.

- Fintech & Insurtech: Wise, Payhawk, Zego, Deel, Rentberry, Fintech-IT Group.

- Cybersecurity & Infrastructure: Avast, AVG, Nord Security, Bitfury, and Unstoppable Domains.

Business models

SaaS remains the dominant business model among CEE scaleups and unicorns, raising 53% of breakout and late-stage VC investment in 2024, according to Dealroom. However, its dominance is slowly declining as investors turn their attention to deeptech and hardware-based solutions.

Physical tech, which includes hardware, IoT, and energy systems, has grown steadily over the past three years, reaching 28% of all scaleups, up from just 4% in 2020. This reflects a broader shift toward tangible innovation in areas such as defence, robotics, energy resilience, and AI-powered devices.

At the same time, marketplace models have slightly rebounded to 19%, signaling sustained investors' interest in scalable digital platforms. Overall, this diversification highlights a maturing CEE ecosystem, moving beyond its SaaS roots toward a more balanced mix of digital and physical innovation.

What’s next

According to Vestbee’s recent data on VC funding in CEE, the region counts over 260 rounds worth more than €1.3 million in the first half of 2025. Capital is becoming more concentrated, as investors favour fewer but larger deeptech and AI-driven deals. This trend marks a shift from broad startup activity toward scaling technically advanced ventures in fields such as AI infrastructure, robotics, and resilience.

From a unicorn perspective, the ecosystem is evolving beyond its traditional SaaS and fintech roots toward deeptech, applied AI, and healthtech. While fintech remains a strong pillar, with new entrants like Fintech-IT Group, the region’s fastest growth now comes from sectors blending software and hardware, including defence, energy, and automation.

A closer look at CEE unicorns of 2024-2025

In 2024, Europe saw a modest rebound in unicorn formation, with 16 European startups reaching the $1 billion valuation mark — up from seven in 2023, but far below the 69 in 2021. The geographic distribution remained concentrated in the continent’s key innovation hubs: the UK, France, the Netherlands, and Germany.

CEE contributed roughly 31% of Europe’s newly minted unicorns, with five companies: ElevenLabs, Creatio, Rentberry, Flo Health, and Mews, surpassing the billion-dollar threshold. All five, however, have their headquarters abroad. While their R&D teams remain rooted in the region, these companies now operate globally, typically from main offices in the US or UK, backed by international investors.

CEE-founded unicorns of 2024:

- ElevenLabs (Poland-founded, UK-headquartered)

In January 2024, the company closed an $80 million Series B, reaching a $1.1 billion valuation and officially joining the unicorn club. Founded in 2022 by two Poles, ElevenLabs develops cutting-edge AI voice synthesis and “voice cloning” tools. Backed by global VC heavyweights such as Andreessen Horowitz and Sequoia, it is now valued at $6.6 billion.

- Creatio (Ukraine-founded, US-headquartered)

In June 2024, Creatio raised $200 million at a $1.2 billion valuation, in a round led by Sapphire Ventures, with participation from StepStone Group, Volition Capital, and Horizon Capital. The company offers a no-code CRM and workflow automation platform. While now headquartered in Boston, Creatio retains significant R&D operations and deep roots in Kyiv. It took the company a full decade to reach unicorn status.

- Rentberry* (Ukraine-founded, US-headquartered)

In September 2024, the rental real estate platform Rentberry raised $90 million from Berkeley Hills Capital and GTM Capital, announcing that its valuation had reached $1 billion. Although based in San Francisco, it was founded by Ukrainians and still maintains strong ties to the region's development.

*Plenty of Ukrainian market observers have questioned whether the valuations reflect the company’s actual scale, pointing to limited traction and revenue visibility.

- Flo Health (Belarus-founded, UK-headquartered)

The women’s health app, founded in 2015 by Belarus-born entrepreneurs, raised over $200 million from General Atlantic in July 2024, valuing the company at above $1 billion. Flo thus became Europe’s first femtech unicorn. Today, its headquarters are in London and its primary development hub is in Vilnius.

- Mews (Czech-founded, Netherlands-headquartered)

The hospitality cloud platform secured a $110 million funding round led by Tiger Global Management, valuing it at $1.2 billion. Though today recognized as one of the fastest-growing Dutch scaleups, Mews’ founding team and technological roots are distinctly Czech.

In 2025, Western Europe continued to lead with 15 new unicorns emerging across the UK, Germany, and the Nordics. Notable new entries included Dren Bio, Loft Orbital, and Namirial. The 2025 unicorn cohort displayed a clear deeptech and healthtech orientation.

CEE added two new billion-dollar companies in 2025:

- Diagnostyka, Poland

In February 2025, Diagnostyka reached a valuation of €1 billion following its IPO on the Warsaw Stock Exchange, with a market cap above PLN 4.4 billion. As Poland’s largest medical diagnostics provider, it stands out as a rare health-focused success in CEE. Though now public, it’s widely included in unicorn discussions due to its scale and regional impact.

- Fintech-IT Group, Ukraine

In March 2025, Fintech-IT Group hit a $1 billion valuation after a growth round led by international investors. The company offers white-label fintech infrastructure and operates globally, with brands such as Fintech Band, Kbyte1024, Shake-to-Pay, and AC DC Processing under its umbrella. Its rise highlights growing interest in embedded finance solutions from CEE.

Together, these cases show that while CEE continues to produce high-quality founders and globally relevant technology, scaling to unicorn status often requires leaving the region.

Who funds CEE unicorns?

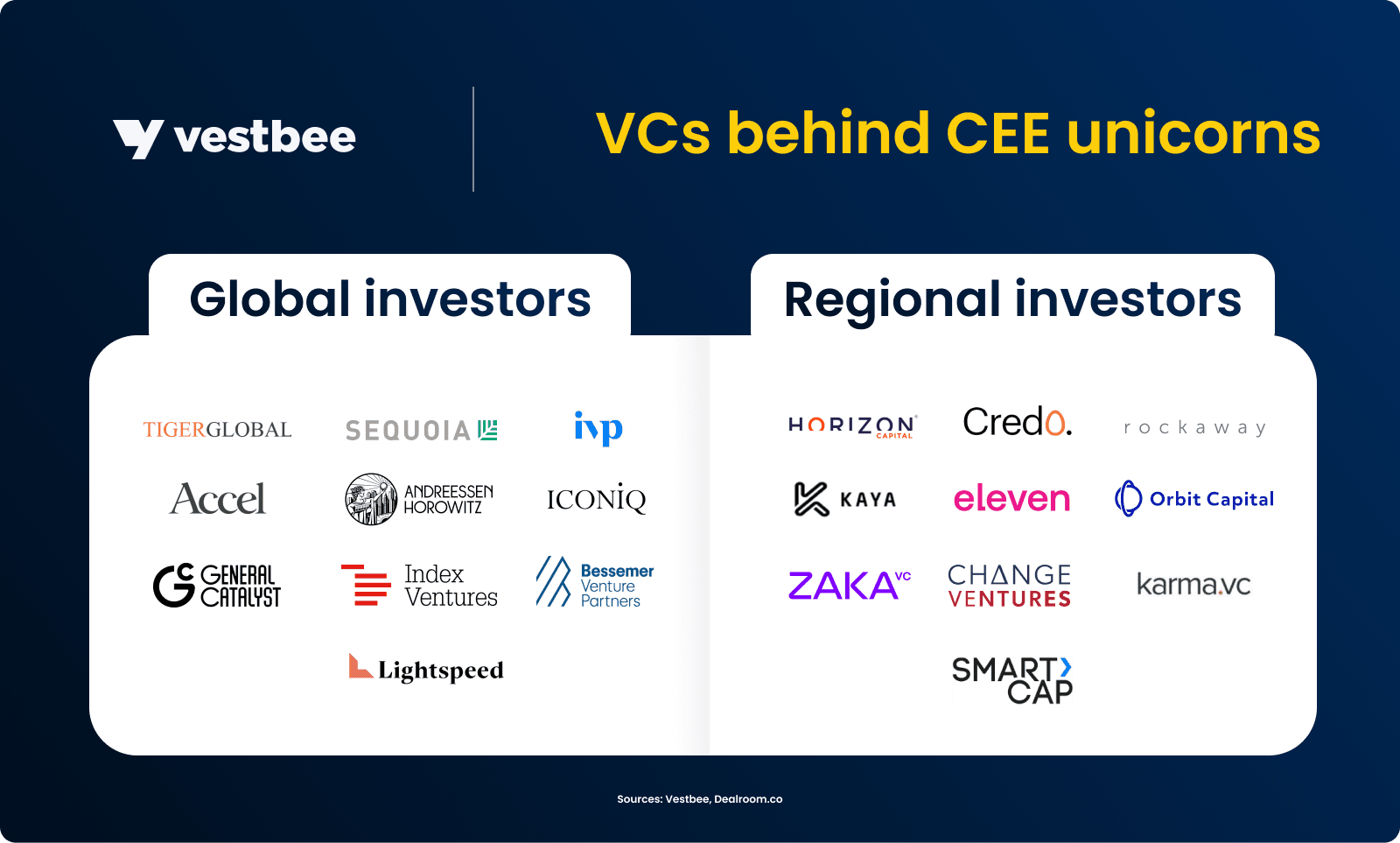

When it comes to VC funding, CEE unicorns reflect a dual structure: early-stage capital driven by regional funds, and late-stage growth overwhelmingly powered by international investors. According to Dealroom and Vestbee data, the most active global investors in CEE-born unicorns include Tiger Global (UiPath, GitLab, Veriff, Mews, Productboard), Sequoia Capital (UiPath, Bolt), IVP (Wise, UiPath, Veriff), Accel (UiPath, Vinted), Andreessen Horowitz (Eleven Labs, Wise, Deel), ICONIQ Growth (Eleven Labs, GitLab), General Catalyst (Grammarly, Zego), Index Ventures (Rohlik, Productboard), Bessemer Venture Partners (Pipedrive), and Lightspeed Venture Partners (Payhawk).

Meanwhile, local VC ecosystems act as the foundation of the unicorn pipeline. Estonia-based Change Ventures, Karma Ventures, and SmartCap have supported future unicorns such as Starship Technologies and Pactum; Credo Ventures (Czechia) backed Productboard and Eleven Labs; Rockaway Capital and Kaya VC invested in Rohlik, Booksy, and Docplanner; while Eleven Ventures (Bulgaria) was an early investor in Payhawk, one of the few locally funded companies to reach unicorn status.

According to Vestbee’s 2025 reports, the most active funds across the region include SMOK VC, Firstpick, Inovo VC, LAUNCHub Ventures, Day One Capital, Tera Ventures, and Startup Wise Guys, reflecting a maturing early-stage infrastructure.

Soon-to-be unicorns

In a joint analysis conducted by Dealroom, Vestbee, Shape Capital Partners, and Cagito Capital, we identified dozens of CEE-founded startups that are on track to join the unicorn ranks in the coming years.

The following ten stand out as the most promising cases:

- Cast.AI (Lithuania, the US) raised $108 million in April 2025 (led by G2 Venture Partners and SoftBank Vision Fund 2), bringing its valuation close to the unicorn threshold amid surging demand for AI-driven cloud-cost automation.

- Stargate Hydrogen (Estonia) secured €42 million in 2024 and another €11 million in early 2025 to scale its ceramic-catalyst electrolyzers for green hydrogen.

- Skeleton Technologies (Estonia) closed a €108 million equity round in 2024 (led by Siemens and Marubeni) and an €18 million EU grant to develop hydrogen-hybrid storage tech.

- Kontakt.io (Poland) raised $47.5 million Series C from Goldman Sachs to expand its AI-powered healthcare IoT solutions.

- ICEYE (Finland, Poland) raised $158 million in 2024 and partnered with Rheinmetall to build SAR satellites.

- FlowX.AI (Romania) closed a record $35 million Series A in 2023 (led by Dawn Capital) — the largest in Romanian history — to help banks modernize legacy systems with AI.

- SEON (Hungary) raised $80 million Series C in 2025 (led by Sixth Street Growth) to scale its anti-fraud SaaS used by Revolut, Plaid, and Spotify.

- Preply (Ukraine) raised $70 million in a Series C extension (2023), led by Horizon Capital, to accelerate the development of AI-enhanced learning tools.

- Lokalise (Latvia) raised $50 million in Series B funding in 2025 to expand localization automation for product teams.

- Omnisend (Lithuania) scaled organically to ~$50–55 million ARR in 2024 with minimal funding, cementing its place as a bootstrapped martech champion.

Beyond the leading scaleups, a broader layer of fast-growing startups is also shaping the region's tech landscape. Emerging players identified by Sifted in its Top 100 DACH & CEE list illustrate the diversity and depth of the ecosystem: AlohaCamp (Poland) is scaling fast in consumer travel and accommodation; Colossyan (Hungary) leverages generative AI for corporate training videos; Turing College (Lithuania) builds an online tech education platform; Spendbase (Ukraine) offers SaaS spend management tools; and Supliful (Latvia) innovates in e-commerce logistics. Many of these scaleups report triple-digit annual growth (200-450% CAGR) while operating with lean funding.

A similar trend appears in Deloitte’s Technology Fast 50 CEE ranking, which highlights the region’s most dynamic and rapidly growing tech companies by four-year revenue growth. Oddin.gg (Czech Republic), a global esports betting technology provider, led the ranking with 7,958% growth, followed by MAGU (Czech Republic), a sustainable consumer-tech brand, and SIA JEFF (Latvia), a fintech building data-driven financial product marketplaces for emerging markets.

Yet, while the region’s scaleup pipeline continues to expand, access to late-stage capital remains a major bottleneck — particularly when compared to Western Europe.

Challenges and opportunities

Late-stage funding remains one of the least developed pillars of the CEE innovation economy. While early-stage activity has grown steadily over the past five years, driven by local accelerators, regional VC funds, and public co-financing, the scaleup gap persists. Only a handful of startups manage to secure $100 million+ rounds needed to achieve global competitiveness, build hardware-heavy infrastructure, or move into adjacent verticals.

The largest CEE-founded rounds in 2025 include:

- Tachyum — Semiconductors / Telecom / AI infrastructure — $220 million Series C — US (Slovakia-founded)

- CyberCube — Cybersecurity / Fintech / Insurance analytics — $180 million Late VC — United States (Estonia-founded)

- MaintainX — Workflow management / Enterprise software — $150 million Series D — US (Romania-founded)

- Cast.AI — Cloud optimization / Enterprise software / DevOps — $108 million Series C — US (Lithuania-founded)

- World Liberty Financial — Fintech / Crypto / DeFi — $100 million late VC — Romania

- Seon — Fraud prevention / Fintech / Security / Regtech — $80 million Series C — Hungary

- Mews — Hospitality tech / Fintech / Property management — $75 million Late VC — Netherlands (Czech-founded)

- Aerones — Robotics / Energy / Clean tech — $62 million Late VC — Latvia

- Greenway Infrastructure — EV charging / Energy / Transportation — €50 million Growth Equity VC — Slovakia

- Pactum — AI / Enterprise software / Automation — $54 million Series C — US (Estonia-founded)

While these figures demonstrate growing investor confidence, they also highlight how concentrated CEE’s late-stage landscape remains. Most of the region’s largest deals are still connected to US-based structures or foreign headquarters, a reflection of how many regional startups relocate to access deeper capital pools.

At the European level, the gap between Western Europe and CEE in late-stage venture funding remained striking. According to Dealroom, the ten largest Western European rounds reached $10.6 billion in total — nearly ten times more than CEE’s $1.08 billion. Revolut’s $2 billion raise alone was almost 9x bigger than Tachyum’s $220 million Series C, the region’s biggest deal.

To overcome the shortage of growth capital, many startups adopt a split-structure approach, maintaining R&D in CEE while basing commercial operations in markets with deeper capital access. It remains one of the most reliable paths to Series B and beyond.

Western Europe continues to lead in complex, capital-heavy innovation such as deeptech, AI, quantum computing, defence, and biotech. In contrast, CEE’s biggest rounds still cluster around fintech and enterprise software, with only a few — like Tachyum’s semiconductor work or Aerones’ robotics, breaking into harder-tech fields.

Still, the region’s funding environment is gradually evolving. Global investors like Accel and Tiger Global are becoming more active in the region, often joining later-stage rounds that were once out of reach for CEE startups. Within the region, growth investors such as Credo Ventures, Orbit Capital, Cogito Capital Partners, Horizon Capital, OTB Ventures, Inovo VC, BlackPeak Capital, and Aspire11 are raising larger vehicles and competing for scaleup opportunities, while early-stage players such as Movens Capital are expanding their focus beyond seed. On top of that, newcomers such as Radix Ventures are targeting deeptech and other underserved verticals.

To explore the investors shaping Europe’s scale-up landscape, see Vestbee’s list of the most active growth-stage VCs, backing startups from Series B onward across Europe and CEE.

The developments of 2025 mark a key opportunity: if the evolution of capital continues to align with the region’s startup maturity, CEE could transition from serving as a launchpad for global ventures to becoming a scaleup destination — one capable of building globally competitive companies that continue to grow and hire within the region.