CEE is one of the fastest-growing startup hubs, with over 3,800 startups and 275 scaleups, outpacing Europe’s growth over the past decade. However, the region faces a paradox: scaling remains a challenge, as highlighted by Louis Geoffroy-Terryn, Head of Research Ops at Dealroom, during the release of a new Dealroom report on the region’s startup ecosystem at the Vestbee CEE VC Summit. Nearly half of CEE scaleups relocate — often to the US — for better access to global markets. Yet, scarce late-stage funding and uneven regional development, particularly in deeptech, could slow the region’s next growth phase.

Vestbee, SHAPE Capital Partners, and Cogito Capital Partners collaborated with Dealroom as co-authors of the report. Below, we highlight its key findings.

Check out the full report HERE.

CEE startup ecosystem has grown by 24.6% since 2022, excluding the record high in 2021

- As of Q1 2025, the CEE ecosystem is worth €243 billion. Over the last five years, it has consistently grown, valued at €180 billion in 2020. 2021 was exceptional, showing a record-high combined enterprise valuation — €269 billion. This was driven by the surge in tech stocks on the public market, with several public CEE unicorns reaching high valuations, including UiPath.

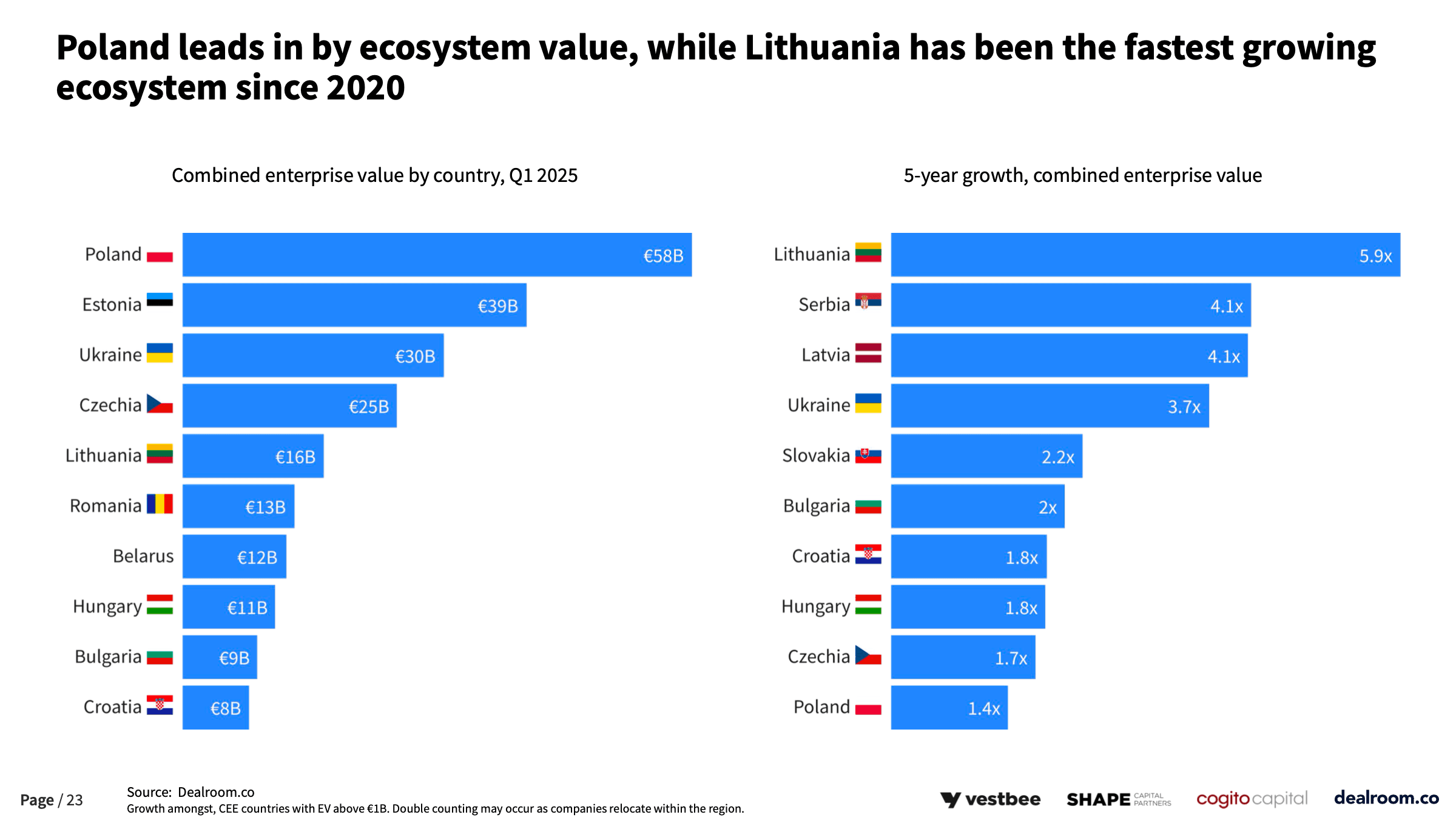

- The top three countries in terms of enterprise value for startups are Poland, Estonia, and Ukraine, contributing €58 billion, €39 billion, and €30 billion, respectively, to the total combined value of the CEE region. Meanwhile, Lithuania has been the fastest-growing ecosystem since 2020.

CEE companies raised €2.3 billion in VC investment in 2024 — €200 million more than the previous year

- This amount includes €764 million as early-stage funding — pre-seed, seed, and Series A, €703 million invested in Series B and Series C, and €818 million — in later stages. After a drop in 2023, late-stage funding has nearly tripled compared to its previous level of €275 million and has surpassed both early-stage and breakout-stage investments.

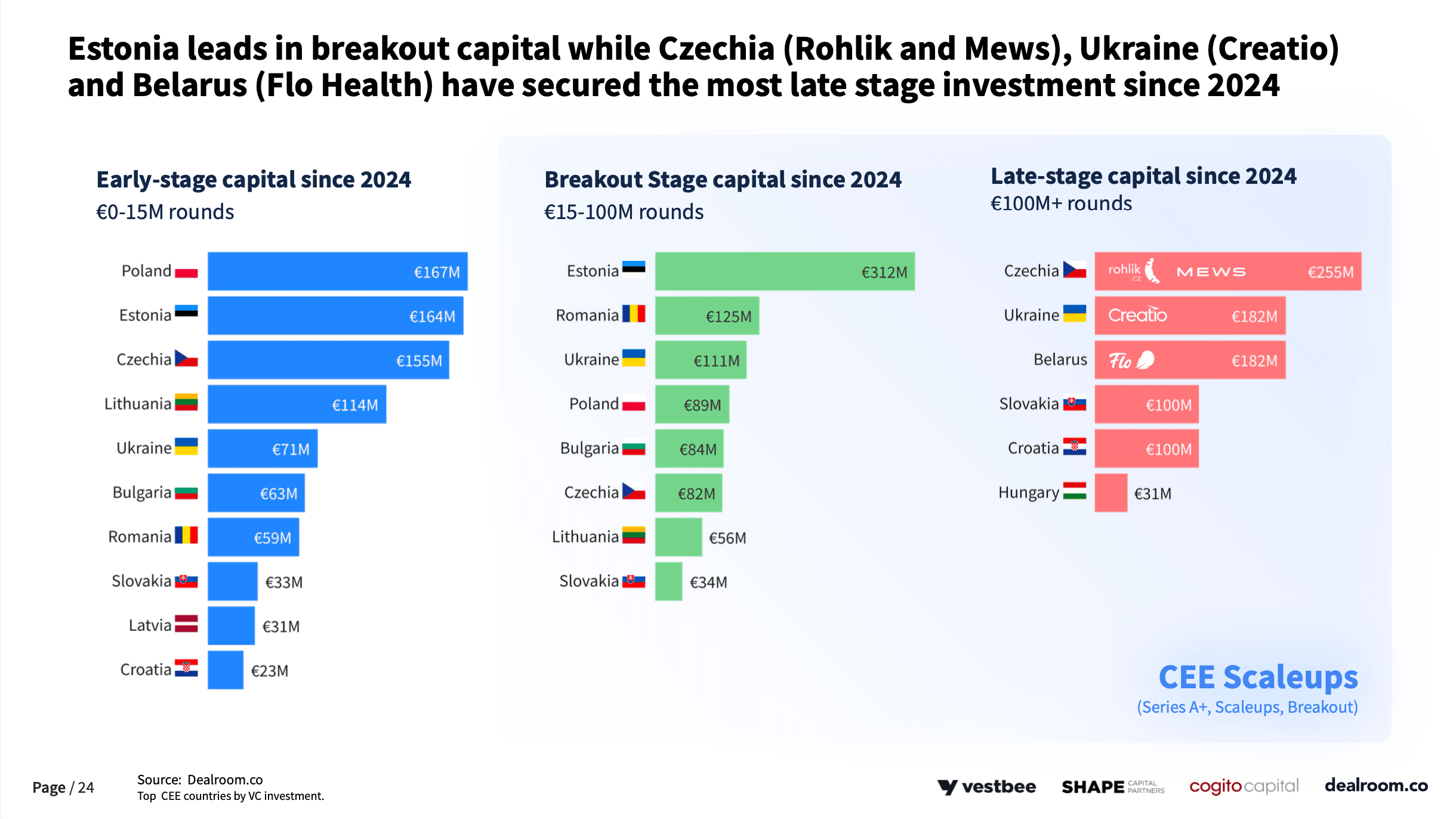

- Poland leads in early-stage capital, having raised €167 million since 2024; Estonia — is in breakout capital with €312 million raised, while the Czech Republic and Ukraine have secured the most late-stage investment — €255 million and €182 million, respectively.

Top rounds in CEE in 2024 included:

- Czech property management system Mews raised €100 million in March;

- Energy tech startup Stargate Hydrogen secured €42 million seed funding in May;

- Ukrainian-founded no-code CRM automation platform Creatio raised €182 million in June.

- Czech online grocery delivery service Rohlik secured €160 million in June.

To learn more about top CEE rounds of 2024, check out Vestbee’s monthly articles series.

CEE scaleup ecosystem is expanding, with Poland leading the ranking

- The report defines 'scaleups' as companies in the breakout, late stage, or unicorn phase. Poland leads the list with 60 such firms, followed by Estonia with 54, the Czech Republic with 38, Ukraine with 26, and Romania with 21.

- In terms of sectors, enterprise software, AI, and fintech dominate the CEE scaleup landscape, with a total of 237 companies in these fields. Deeptech, climate tech, marketing, blockchain, transportation, energy, and security also rank among the top ten prevailing industries.

- The ranking of verticals by funding looks different — transportation, fintech, and energy are the most funded sectors in CEE in 2024, with €436.7 million, €378.5 million, and €343.7 million raised, respectively.

- SaaS remains the dominant business model, while physical tech has been developing over the past year, reaching its highest percentage since 2020 —28%, compared to 4% in 2020 and 22% in 2023.

- At the same time, 48% of CEE scaleups have been relocated, with Ukrainian companies having the highest relocation rate. 56% of companies moved to the US, 39% moved to other European countries, including 24% to the UK.

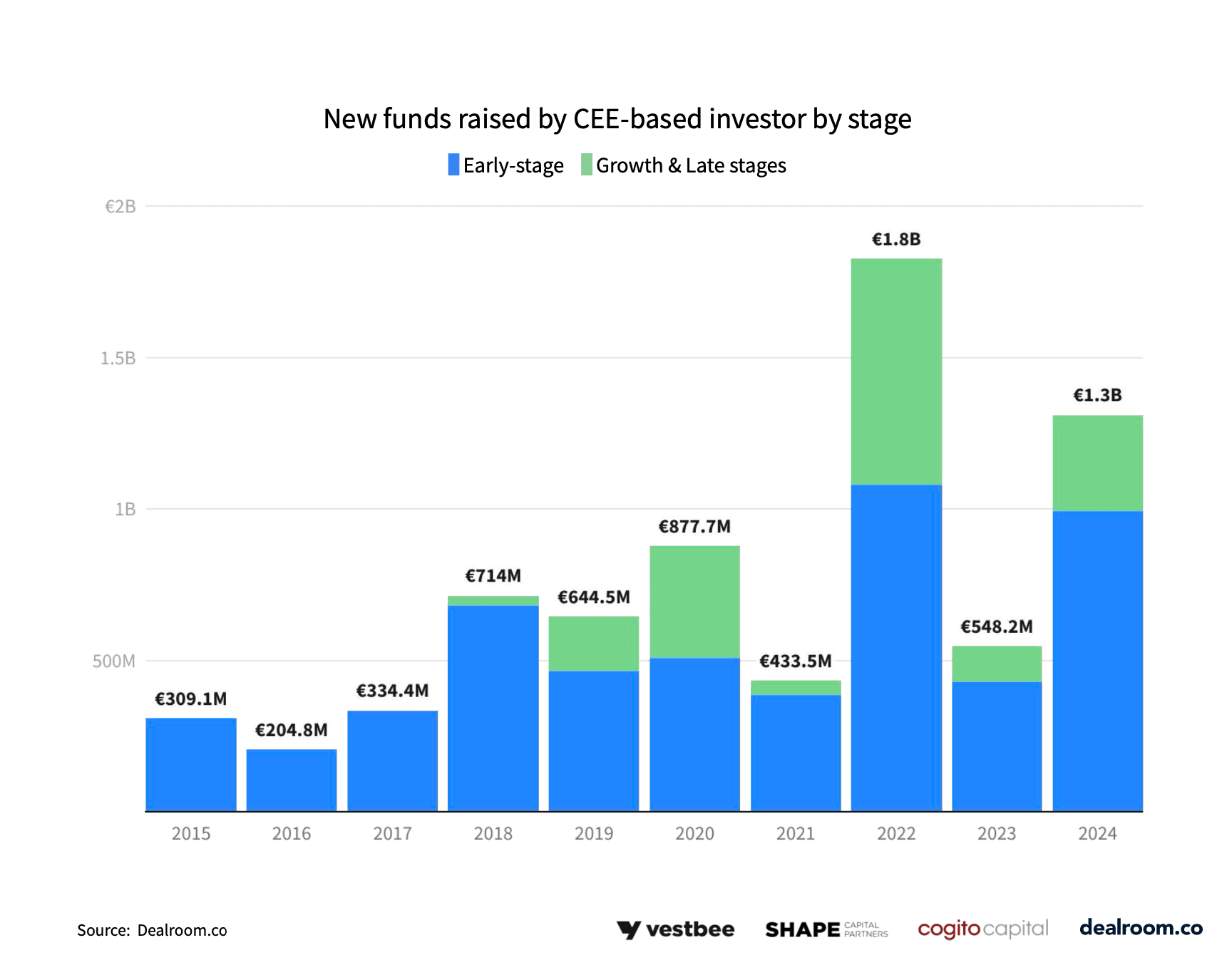

CEE raised €1.3 billion in new funds in 2024

- In 2024, the region saw the second-highest VC fundraising ever, following 2022, which reached €1.8 billion. In 2023, the total was €548.2 million.

Top new funds launched in 2024 include:

- Horizon Capital raised €318 million for Growth Funds IV.

- Cogito Capital secured €90 million for Fund II.

- Lead Ventures launched €100 million for Fund III.

- OTB Ventures closed a €168M Fund II.

- Presto Ventures introduced €150 million for Presto Tech Horizons Fund.

To learn more about VC fundraising of 2024, check out Vestbee’s blog.

- Since 2010, the most active early-stage investors have been Hungarian Hinvestures, Bulgarian Innovation Capital and Vitosha Ventures Partners, Croatian Fil Rouge Capital, and Czech Credo Ventures.

- The top 10 most active Series B+ investors since 2020 are mostly foreign, with 50% represented by US funds, including Bessemer Venture Partners, Tiger Global, Insight Partners.

Find out more about the most active investors backing European companies at the growth stage of their development in our collection of 60 funds.