Welcome to the September 2025 edition of the CEE SaaS Index, developed by Warsaw Equity Group and Vestbee to provide a clear, region-specific benchmark for valuing SaaS companies in Central and Eastern Europe. The following index aims to help founders, investors, and members of the local startup ecosystem track valuation trends, compare regional performance with global benchmarks, and better understand the forces shaping the future of SaaS in CEE.

SaaS remains among the most funded verticals, despite low deal activity in Europe

Investor activity in Europe remained subdued in Q3 2025, with 2344 deals recorded, according to PitchBook’s European Venture Report, which represents a decline from 2500-2900 deals in the first two quarters of the year. Despite the slowdown, SaaS remains one of the most well-funded verticals, ranking second only to AI and machine learning. The year-to-date venture deal value in Europe is estimated at €43.7 billion, with CEE accounting for roughly 5-6% of the total raised capital, and it continues to increase in recent years.

Strong equity momentum supporting SaaS valuations

Global equity markets entered Q3 2025 in a clear bull phase. The WIG index on the Warsaw Stock Exchange reached record highs above 112,000 points, while the Nasdaq Composite in the US also set a new all-time peak. Investor optimism around AI has lifted companies' valuations, supporting the continued growth of the CEE SaaS Index.

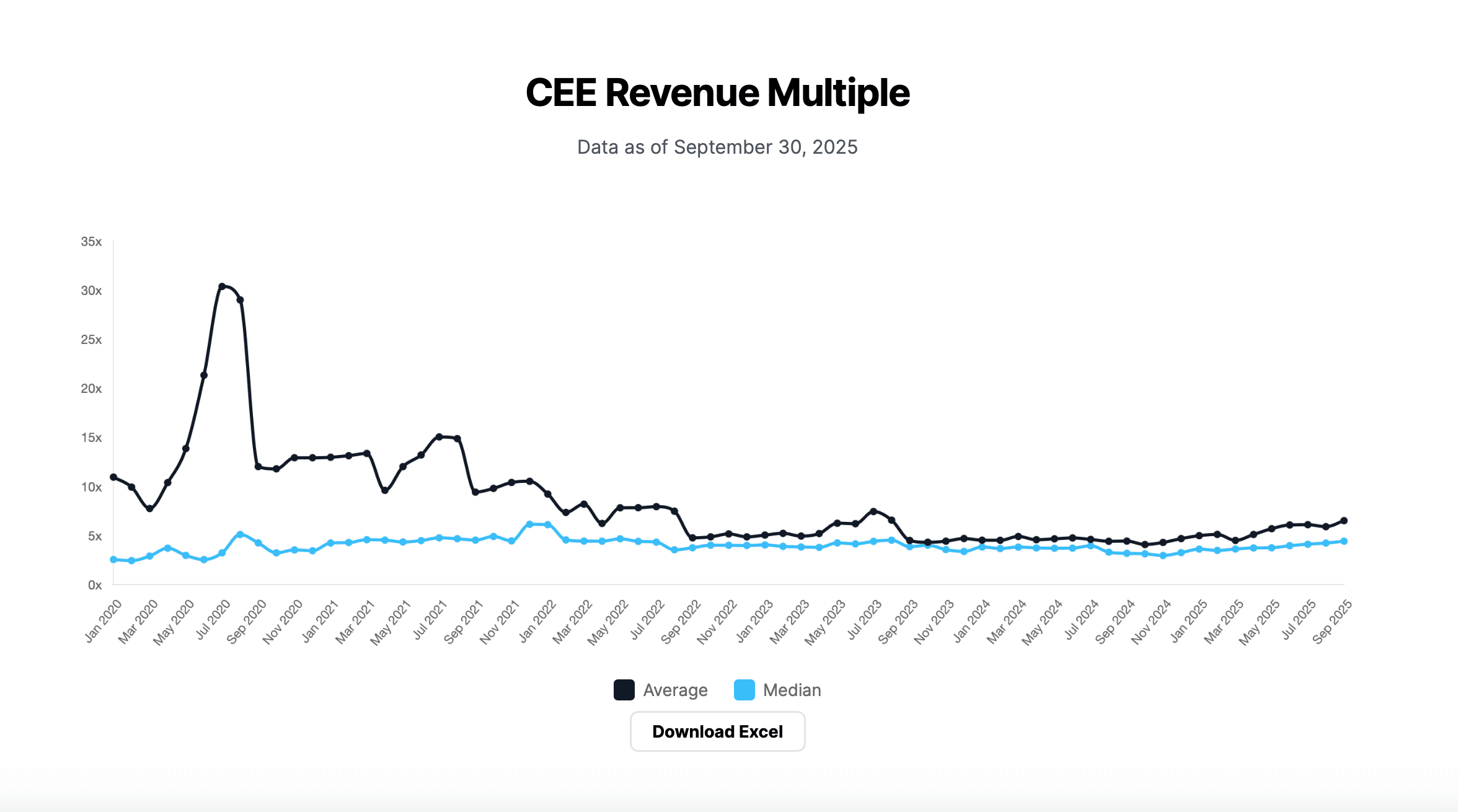

CEE SaaS index reached its highest level

The CEE SaaS Index achieved its highest historical level in September, surpassing a €2.2 billion valuation. This marks another consecutive record quarter, despite two companies being delisted since the index’s inception. The median revenue multiple in the CEE region increased to 4.45x, representing 39% year-on-year growth, while the median annual revenue growth rate declined by 2.8 percentage points, to 4.5%.

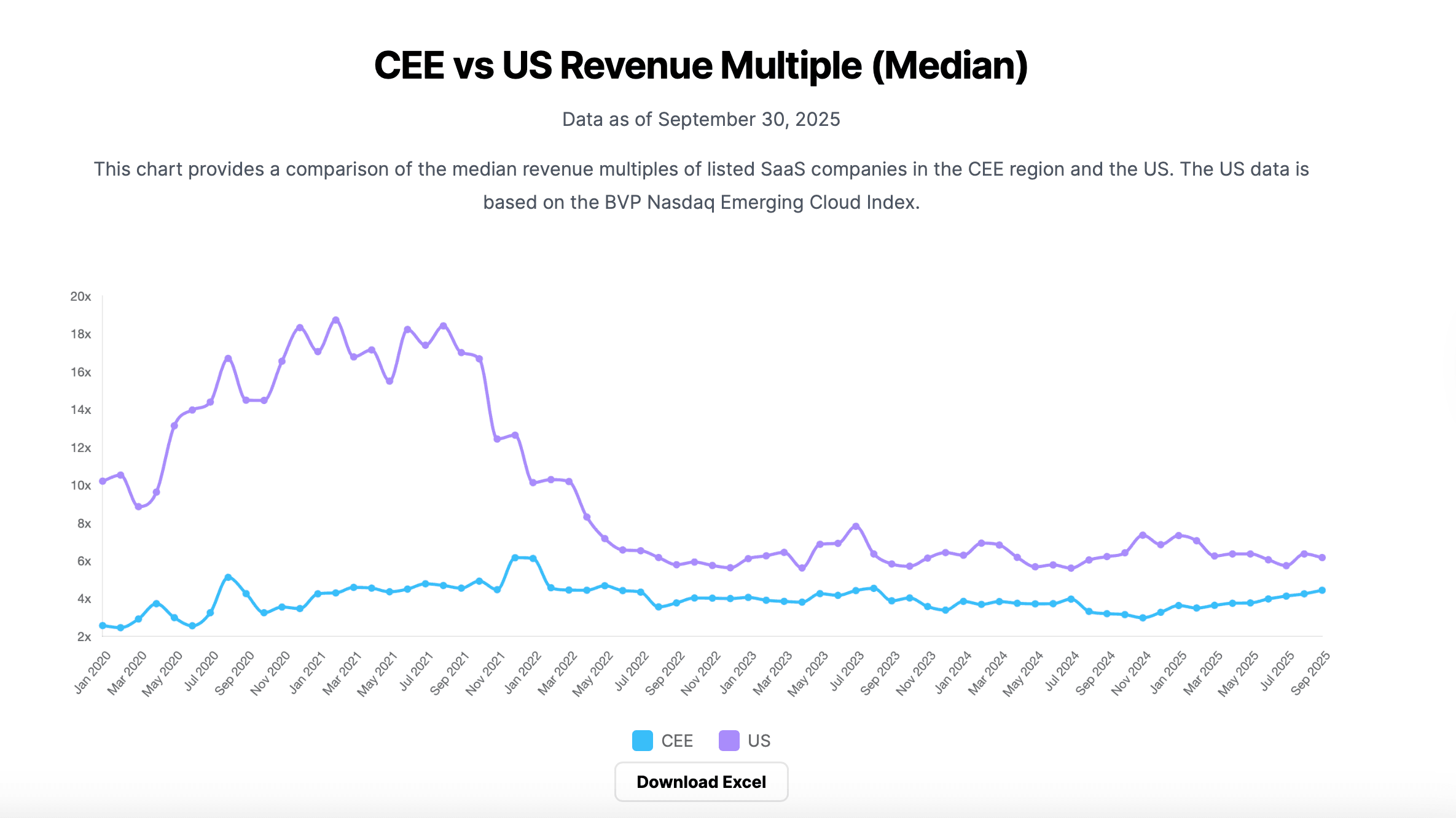

Narrowing the gap to the US multiples

The valuation gap between CEE and US SaaS companies continues to narrow. The median revenue multiple for CEE SaaS companies reached 4.45x in Q3 2025, compared with 6.18x for US peers in the BVP Cloud Index. This represents a 28% discount, a 21 percentage point decrease from 49% a year ago. However, revenue growth rates remain the key differentiator: US SaaS companies continue to expand revenues at a median pace of 19% year-on-year, compared with just 4.5% among CEE companies.

About CEE SaaS Index

CEE SaaS Index is a simple tool for startups and investors to value SaaS companies in Central & Eastern Europe based on revenue multiples from publicly traded SaaS companies from the CEE region, developed by Vestbee and Warsaw Equity Group.

While revenue multiples from publicly traded SaaS companies can provide a helpful starting point for valuation, currently available indexes are only based on US-listed SaaS companies, leaving the CEE region without relevant benchmarks, despite the region's thriving startup ecosystem and quadrupled VC funding over the last three years.

With projected growth and increased investment in CEE tech companies, a more appropriate valuation benchmark for regional startups and investors is required. To meet this need, Vestbee and the Warsaw Equity Group have collaborated to develop the CEE SaaS Index, providing a relevant benchmark for regional and international investors.

Key updates on CEE SaaS Index performance for Q3 2025:

- CEE SaaS Index valuation reached €2.2 billion, marking another record high

- Median revenue multiple in CEE increased to 4.45x, up 39% year-on-year.

- The CEE-US SaaS valuation gap narrowed to 28%, improving by 21 percentage points compared to last year.

- Median annual revenue growth rate among CEE SaaS companies declined to 4.5%, versus 19% in the US.