Key takeaways

- Global venture funding in Q3 2024 totaled $66.5 billion, marking a sustained decline with a 16% drop quarter-over-quarter and 15% year-over-year, driven by reduced late-stage mega-deals and slower VC fundraising, while early-stage funding remained flat, underscoring a cautious and resource-constrained venture landscape with limited signs of recovery.

- Venture funding to European startups in Q3 2024 plummeted to $10 billion, the lowest since Q3 2020, with a 36% quarter-over-quarter and 39% year-over-year decline, reflecting widespread challenges in the European startup ecosystem; while Germany showed resilience with a 33% funding increase, late-stage funding hit multi-year lows, and early-stage and seed activity contracted, emphasizing the need for renewed investor confidence and ecosystem support.

- Venture funding in Central and Eastern Europe saw a sharp decline in Q3 2024, with total funding dropping 35% year-over-year to €360 million and the number of rounds plunging 54% to just 118, driven by tough macroeconomic conditions, reduced activity from both international and local investors, and the absence of mega-rounds, leaving startups in the region facing prolonged fundraising cycles, stricter deal terms, and a growing risk of stagnation.

Global VC investment trends

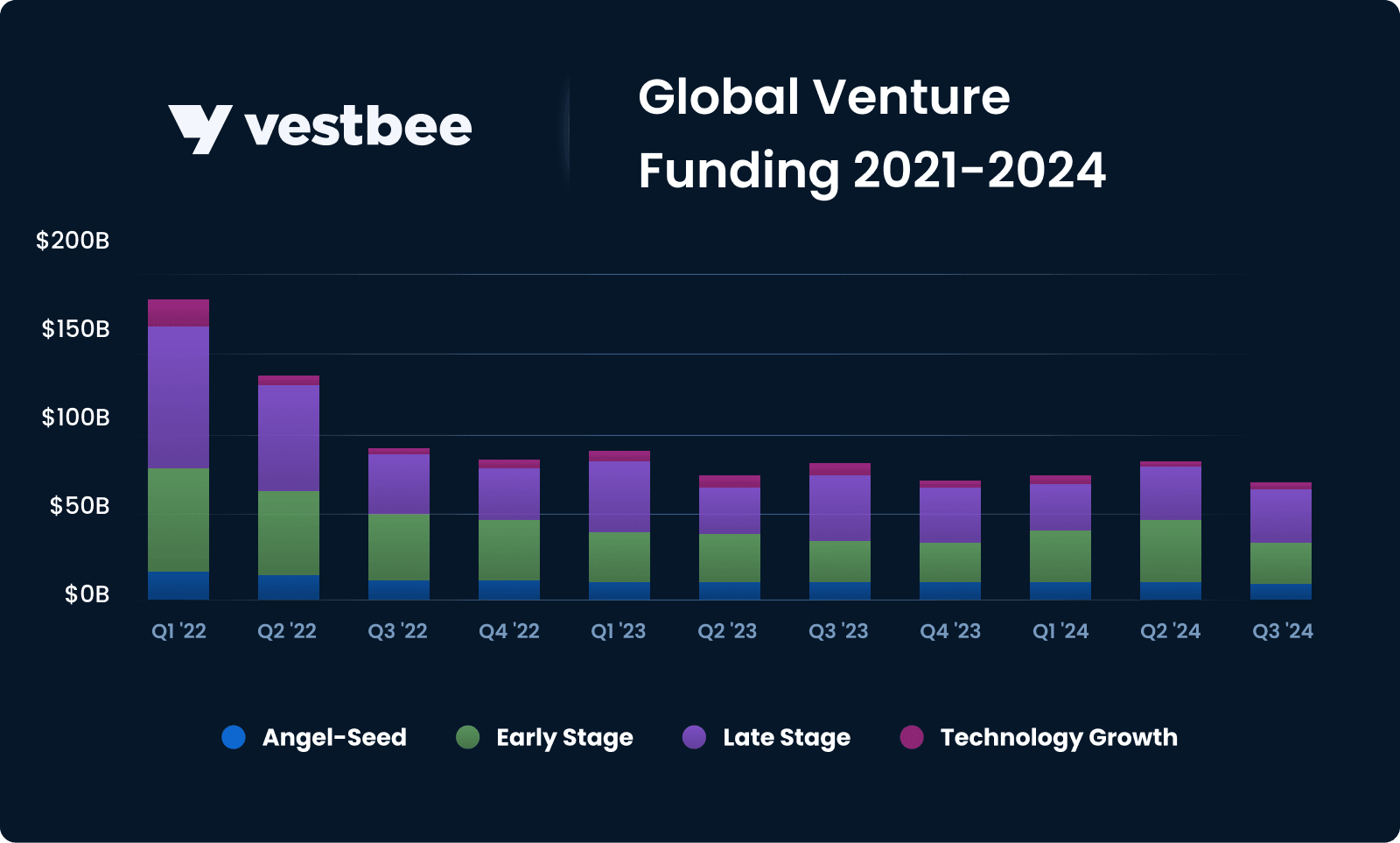

Global venture funding in Q3 2024 totaled $66.5 billion, according to Crunchbase data, representing a 16% decline quarter-over-quarter and a 15% decrease compared to the $78 billion invested in Q3 2023. This marks the ninth or tenth consecutive quarter of decline in global startup funding, underscoring the sustained downturn in the venture landscape.

This past quarter is only the second since the onset of the funding slowdown to dip below the $70 billion threshold, a level not seen since 2017 apart from Q4 2023. While these figures point to a subdued funding environment, they do not necessarily indicate a further contraction moving forward, as fluctuations influence quarterly totals in large funding rounds.

Late-stage funding in Q3 2024 reached $34.7 billion, remaining flat quarter-over-quarter but down sharply from $46 billion in Q3 2023. The most significant decline was observed in deal activity exceeding $500 million, reflecting a continued hesitancy among investors to commit to large-scale, late-stage investments. Notable late-stage funding rounds targeted sectors such as autonomous driving, defense technology, professional services, semiconductors, and AI models during the quarter.

Early-stage funding totaled $24.7 billion, down sequentially, largely due to the absence of outsized deals like the $6 billion Series B round for xAI in Q2 2024, which had skewed prior numbers upward. Year-over-year, however, early-stage funding remained flat, with large rounds concentrated in AI and biotech, underscoring sustained investor confidence in these innovation-driven sectors.

Year-to-date, global venture funding is down approximately 7% compared to the same period in 2023. While seed funding appears flat and may show a slight uptick as additional rounds are disclosed post-quarter, early-stage funding has risen by 10% year-over-year. In contrast, late-stage funding has declined by approximately 20%, driven by reduced capital deployment in mega-deals.

These trends highlight a shifting dynamic within the venture ecosystem. While overall activity seems to be stabilizing, the pace of fundraising for venture funds has slowed significantly in 2024. This contraction in available capital will likely exert downward pressure on the earliest stages of funding, creating challenges for startups seeking to establish themselves in an increasingly competitive and resource-constrained environment. The data suggests that the venture industry remains in a cautious holding pattern, with limited indications of a robust recovery in the near term.

VC investment trends in Europe

Venture funding to European startups reached $10 billion in Q3 2024, marking the lowest quarterly total since Q3 2020, according to Crunchbase data. This represents a dramatic decline of 36% quarter-over-quarter and 39% year-over-year, underscoring the mounting challenges the European startup ecosystem faces amidst the prolonged global VC downturn.

Among Europe’s three largest markets for venture capital, Germany stood out as the only country to record both quarter-over-quarter and year-over-year growth, signaling localized resilience in an otherwise contracting funding environment. Meanwhile, the UK, traditionally Europe’s leading destination for venture capital, saw funding plummet by 43% year-over-year to $3.2 billion. France, typically the continent's second-largest market, dropped to $1.4 billion in investments, falling behind Germany, which experienced a notable 33% increase to $2.4 billion.

Late-stage funding across Europe reached $4.2 billion in Q3 2024, spread across more than 70 rounds, reflecting a steep 57% year-over-year decline. This sharp contraction highlights a growing hesitancy among investors to commit significant capital to mature startups, likely driven by tightening market conditions and increased scrutiny of late-stage valuations.

Early-stage funding fared slightly better, totaling $4.5 billion across just over 290 rounds. While early-stage activity demonstrates relative stability, the overall decline in venture activity limits opportunities for new companies to progress into later stages. Seed funding also showed signs of weakness, falling to $1.5 billion across 800 rounds — a reduction from the $1.8 billion recorded in Q3 2023. However, given that seed-stage deals are often reported after the quarter’s close, these figures may see modest upward revisions.

Despite the grim figures, it’s worth noting that European venture investment since the start of the VC downturn has exhibited fluctuations, ranging from $12 billion at its prior low to nearly $17 billion at its high. Q3’s underperformance does not preclude the possibility of a rebound in Q4, especially if macroeconomic conditions stabilize and investor sentiment improves.

In summary, while Germany's resilience offers a rare bright spot, the overall funding environment in Europe remains under significant pressure. With late-stage funding at multi-year lows and early-stage and seed activity also contracting, the data underscores the urgent need for revitalization in the European venture ecosystem to support sustained innovation and growth.

VC investment trends in CEE

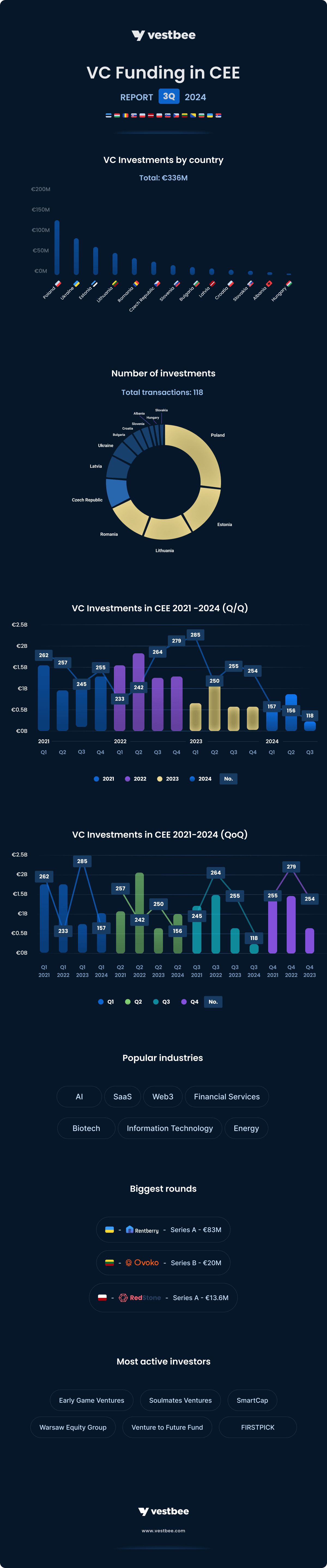

A year-over-year comparison of Q3 2023 to Q3 2024 paints a stark picture of the deteriorating venture capital landscape in Central and Eastern Europe (CEE). Total funding value plummeted from €560 million to €360 million, marking a 35% decline. Even more troubling is the sharp drop in the number of funding rounds, which fell from 255 in Q3 2023 to just 118 in Q3 2024 — a staggering 54% decrease. These figures underscore the deepening challenges for startups in the region, as both early- and late-stage companies struggle to secure investment in an increasingly constrained funding environment.

The decline reflects a combination of factors, including tougher macroeconomic conditions, ongoing geopolitical uncertainty, and reduced foreign and local funds activity. International investors, historically key players in the region’s growth, appear more cautious, reallocating resources to perceived safer markets. Simultaneously, local funds face their own constraints, with limited dry powder and fewer opportunities for follow-on investments. This dual pullback has created a funding vacuum, leaving startups with fewer options for scaling and sustainability.

Another alarming trend this quarter has been the complete absence of mega-rounds — large funding rounds typically driven by mature startups in the region. This indicates that even established companies, which usually command greater investor confidence, face headwinds in attracting substantial capital. The lack of such rounds not only drags down total funding figures but also signals broader hesitancy from investors to back high-growth ventures at scale.

These developments highlight a critical shift in the CEE ecosystem. Startups now face longer fundraising cycles, increased scrutiny, and tougher deal terms, which could hinder innovation and limit the pipeline of scalable ventures in the region. Without a resurgence in investor confidence and activity, the CEE venture ecosystem risks stagnation, further widening the gap between it and more developed markets in Western Europe and beyond.

Startup investment rounds in CEE in Q3 2024

> Number of funding rounds: 118 (98 fully disclosed in terms of amount, month, investors, and company details)

> The biggest disclosed investment rounds: Rentberry, a €83M Series A, Ovoko, a €20M Series B, RedStone, a €13.6M Series A round

>Total value of funding closed in CEE: over €360M*

> Countries with the highest number of funding rounds: Poland — 45 rounds, Estonia — 16, Lithuania — 14 rounds

> The most active VC funds: Early Game Ventures, SmartCap, Soulmates Ventures, FIRSTPICK, Venture to Future Fund, Warsaw Equity Group

> The most popular industries: Financial Services, AI, SaaS, Energy, Web3, Information Technology, Biotech.

*20 rounds undisclosed in terms of transaction value

What shaped the CEE ecosystem in Q3 2024

In Q3 2024, the Central and Eastern European (CEE) venture capital ecosystem recorded 118 transactions, with deal activity steadily increasing month by month—27 in July, 31 in August, and 40 in September. While this upward trend within the quarter is encouraging, it takes place against a backdrop of a significantly contracted market compared to previous years.

Among the largest disclosed rounds this quarter were Ukrainian-founded (US-based) Rentberry’s €83 million Series A, Lithuanian Ovoko’s €20 million Series B, and Polish RedStone’s €13.6 million Series A.

Geographically, Poland, Estonia, and Lithuania dominated the activity, leading the region with 45, 16, and 14 funding rounds, respectively. Together, these three countries accounted for most of the deal flow and secured nearly 50% of the total capital raised in Q3, cementing their position as the central hubs for venture activity in the CEE region. Ukraine also played an important role, contributing over 20% of the quarter’s funding volume, driven primarily by Rentberry’s round.

Investor interest this quarter gravitated toward sectors such as Financial Services, AI, SaaS, Energy, Web3, Information Technology, and Biotech. These areas reflect where the market perceives the highest growth potential, although the overall level of activity across these sectors has declined compared to previous years. The continued focus on emerging technologies and scalable solutions suggests that while the region faces significant challenges, it still holds pockets of resilience and innovation.

Now, let's discover the note-worthy and recently raised VC funds from CEE.

New VC funds from CEE in 3Q 2024:

- Budapest-based VC Lead Ventures has launched a €100 million fund to support CEE startups in late seed and Series A rounds.

- Sofia-based VC BrightCap has completed the first close of its new fund, BrightCap II, targeting €60 million. It will invest in startups focusing on the future of work, digital health, and fintech across SEE.

- Polish fund investor PFR Ventures has invested €47 million (PLN 200 million) in four early-stage VC firms: 24Ventures, Digital Ocean Ventures Starter, Hard2beat, and Tar Heel Capital Pathfinder.

Interested in other new VC funds investing in CEE and Europe? Check out our article New VC Funds Investing in Europe — 3Q 2024.

Let's take a closer look at the Q3 results on a month-by-month basis. However, this review was solely based on fully disclosed rounds (name of startup, closing date, round’s size, participating investors).

Investment rounds in September

> Number of funding rounds: 40

> The biggest investment rounds: Rentberry, a €83M Series A, Ovoko, a €20M Series B, PastPay, a €12M Series A round

> Total value of funding secured in CEE: over €216M

> Countries with the most funding rounds: Poland — 10, Romania — 8.

> The most active VC funds: Early Game Ventures, Warsaw Equity Group, Soulmates Ventures

> The most appreciated industries: AI, Financial Services, Information Technology.

In September 2024, the CEE startup ecosystem demonstrated the most significant activity, accounting for nearly 60% of the total funding activity in Q3. The month saw over €216 million invested across 40 disclosed funding rounds, representing a high point for the region's quarterly performance. Poland and Romania emerged as the leading contributors in terms of the number of transactions, recording 10 and 8 funding rounds, respectively. These two markets, along with Lithuania, were key drivers of total funding value. Lithuanian startups alone raised over €22 million, showcasing the country's growing influence within the region.

However, the month's exceptional funding volume was heavily influenced by a single transaction: the €83 million round raised by Rentberry, a Ukrainian-founded but US-based platform. Excluding this significant deal, the overall funding landscape in September would have been considerably more modest, underscoring the pivotal role of landmark rounds in shaping ecosystem metrics.

Year-over-year, September 2024 reflects mixed trends. While the total funding amount, adjusted for Rentberry, remains on par with the same period in 2023, the number of deals has declined sharply by 50%, signaling a potential contraction in early- and growth-stage activity across the region.

This month's most active sectors were Artificial Intelligence, Financial Services, and Information Technology, further emphasizing investor preference for scalable, tech-driven solutions. Among the most notable investors were Early Game Ventures, Warsaw Equity Group, and Soulmates Ventures, all of which maintained a strong regional presence. GTM Capital and Berkley Hills Capital also made significant contributions, mainly through their involvement in Rentberry's almost-mega round, underscoring their strategic interest in high-impact, cross-border opportunities.

This data underscores a key narrative for the CEE region: while biggest deals can elevate aggregate funding figures, the broader ecosystem may face challenges in sustaining deal volume — a metric critical for fostering long-term innovation and ecosystem health.

Find out more: TOP CEE funding rounds closed in September.

Investment rounds in August

> Number of funding rounds: 31

> The biggest investment round: MMI, a €7.7M venture round, Biomatter, a €6.5M Seed round, Bourgebois Boheme, a €6.5M Seed round.

> Total value of funding secured this in CEE: over €55M

> Countries with most funding rounds: Poland — 8, Estonia — 6 rounds

> The most active VC funds: Practica Capital, Czech Founders VC

> The most appreciated industries: Financial Services, AI, Biotech, IT.

August marked the least active month of Q3 2024 in terms of total funding value, with just over €55 million raised across 31 disclosed rounds. Among the standout transactions were a €7.7 million venture round into Poland’s MMI, as well as two €6.5 million seed rounds secured by Lithuanian startups Biomatter and Bourgebois Bohème.

Geographically, Poland and Estonia led the region in the number of deals, recording 8 and 6 rounds respectively. However, Lithuania emerged as the dominant player in terms of total funding value, raising over €15 million — nearly 30% of the month’s total. This underscores Lithuania’s growing reputation as a hub for venture activity within the CEE region.

On the investor side, Practica Capital and Czech Founders VC were among the most active participants in August, contributing to deals across the region. The funding rounds largely concentrated on sectors such as Financial Services, AI, Biotech, and Information Technology, which remain consistent priorities for both regional and international investors.

Despite these pockets of activity, August’s performance underscores the ongoing challenges facing the CEE venture ecosystem. Historically, the summer months are slower across Europe due to seasonality; however, this year’s results reflect a sharper decline. Compared to August 2023, there was a significant drop of over 40% in the number of funding rounds and a 35% decrease in total funding value. This contraction highlights persistent headwinds for the VC and startup ecosystem, including tighter capital availability and a cautious approach from investors amid broader economic uncertainty. These figures suggest that the region’s recovery remains uneven, and further measures may be needed to stimulate deal activity in the coming months.

Find out more: TOP CEE funding rounds closed in August.

Investment rounds in July

> Number of funding rounds: 27

> The biggest investment round: RedStone, a €13.6M Series A round, eAgronom, a €10M Series A round, Leanpay, a €10M Series B round.

> Total value of funding secured in CEE: over €67M

> Countries with the most funding rounds: Poland — 7 rounds, Romania — 5 rounds.

> The most active VC fund: Venture to Future Fund

> The most appreciated industries: Web3, AI, SaaS.

In July, startups across Central and Eastern Europe raised just over €67 million through 27 disclosed rounds, marking another challenging month for the region's venture ecosystem. While Poland and Romania led the way with 7 and 5 rounds respectively, the overall activity reflects a sharp downturn compared to historical norms, as both deal volume and total funding continue to dwindle.

Among the few notable rounds were Polish RedStone’s €13.6 million Series A, Estonian eAgronom’s €10 million Series A, and Slovenian Leanpay’s €10 million Series B. However, these transactions stand as exceptions in an increasingly difficult market. Investors primarily focused on AI and SaaS, but their appetite appears limited, with fewer high-value deals and a shrinking pool of available capital.

The most active investor this month, Venture to Future Fund, played a significant role in the region, alongside an unusually large syndicate participating in RedStone’s Series A, which included Arrington Capital, SevenX, IOSG, Spartan Capital, and others. This deal accounted for a substantial share of the month’s total funding, highlighting the heavy reliance on a small number of rounds to prop up aggregate figures.

The data paints a concerning picture for the CEE ecosystem. Compared to July 2023, the number of rounds has dropped by over 55%, while the total funding amount has plummeted by a staggering 77%. This sharp decline signals deeper structural issues, as investor caution, economic uncertainty, and constrained capital availability take a severe toll. The region's startup ecosystem is struggling to sustain momentum, with fewer opportunities for early- and growth-stage companies to secure critical funding.

Find out more: TOP CEE funding rounds closed in July.

Now, look closer at the top 50 funding rounds closed in CEE between July and September 2024.

Top 50 CEE startup funding rounds closed in Q3 2024:

- Shen.AI offers app & tele-health integration for remote vital sign checks, aiding health providers in delivering complete care online.

- SATIM specializes in object detection and classification using SAR satellite imagery.

- Ogre AI is a data science startup that engages in artificial intelligence and machine learning solutions for the utility industry.

- MMI manufactures high-quality tourist and city buses using IVECO and Mercedes chassis, offering both diesel and compressed natural gas (CNG) power options.

- Electrify, produces electric buses, minibusses, and provides charging infrastructure solutions.

- dotLumen is a health-care startup that uses AI, robotics, and neuroscience to empower the blind.

- Codery is a platform that leverages AI to source, evaluate, and match remote developers to a company's needs.

- Synerise is a cutting-edge AI-driven infrastructure tailored for collecting, analyzing, and interpreting behavioral data.

- Ovoko is an online marketplace that connects sellers of car parts, auto dismantlers, and recyclers with dealers, mechanics, and enthusiasts.

- RedStone creates a multichain database that provides pricing information for smart contracts and DeFi protocols.

- PastPay is a FinTech startup that provides payment processing platform which offers instant payments to businesses and flexible Buy Now, Pay Later (BNPL) options to their B2B customers.

- eAgronom aims to help farmers adopt sustainable practices for the health of their soils and the planet.

- AIO develops sustainable alternatives to animal fats, palm and coconut oil.

- Youni uses AI to streamline university admissions for students.

- Yedem nimble all-mobility solutions for happier employees and a happier planet.

- UP Catalyst produces sustainable carbon nanomaterials and graphite for the green energy storage industry.

- Talkie.ai improves efficiency of Patient Access using AI-based phone virtual assistants.

- RobosizeME assists hotel chains and large hospitality management companies in enhancing operational efficiencies across all hotel operations.

- Rapid Delivery Analytics digital shelf analytics solution specifically designed for mobile-first rapid grocery and convenience delivery services.

- Petsy is a marketplace that connects pet parents with local petsitters.

- Mifundo AI-based platform which makes cross-border lending possible for the banks and consumers in the EU.

- Legit provides an End To End privacy automation platform that solve compliance problems.

- Jeff is a broker of personalized loan products, connecting borrowers and lending institutions.

- Granta Autonomy develops autonomous recon drones, lightweight gimbals, and digital datalink software.

- Fairown is on a humble mission to make the world a 100X better place, one sustainable purchase at a time.

- Doctor.One is a next-generation virtual clinic, helping any doctor build a subscription-based private practice.

- The Cat Health Company focuses on cats health research to prevent or delay age-related illnesses in cats.

- Biomatter is a synthetic biology company that creates new proteins for health and sustainable manufacturing applications.

- Airvolve is developing a heavy-lift aircraft designed for civil and defense missions, offering ten times lower operating costs than a helicopter.

- Adam is a platform connecting homeowners and businesses with verified local professionals.

- Tingit is a zero-effort repairs marketplace for busy people & brands.

- Pentra provides an out-of-the-box platform for logging actions and automatically writing reports using generative AI.

- Blocksense is a decentralized and unrestricted protocol that consumes Oracle data feeds.

- Revoize provides noise reduction and speech enhancement technologies.

- Rentberry is a platform for real estate rental and management.

- Leanpay develops Buy Now Pay Later 3.0, providing innovative installment payment solutions for vendors and consumers.

- Oxla builds a next-generation OLAP database that delivers extremely fast and efficient data processing.

- Kodano manufactures and distributes lenses and eyewear.

- Authologic provides a platform that enables businesses to automate identity checks using government-issued e-IDs.

- Pergamin is an online draft & sign platform that makes it easy to create, negotiate and manage contracts.

- Xopero is a provider of backup & disaster recovery software.

- Rift is a sales platform focusing on automating repetitive and tedious sales work.

- Sloneek provides an innovative all-in-one HR solution.

- Digital First AI is a marketing software that leverages AI to optimize plans and produce advertising materials, saving time and maximizing budgets.

- Eany.io develops a B2B platform designed to simplify the trade of electronics, household items, and DIY products.

- Assisterr aims to change the AI industry by leveraging the Solana blockchain to develop small language models (SLMs).

- AISPECO manufactures advanced geospatial data collection platforms with multi-sensor payloads, combining LiDAR and hyperspectral imaging for airborne, mobile, and stationary use.

- Certific develops a platform that improves communication between doctors and patients by blending medical insights with advanced technology.

- CBRX offers a platform for automating incident analysis, tailored for cybersecurity professionals.

- The Linghos develops an AI-based speech therapy app for kids. The app diagnoses speech impediments, recommends personalized therapy, and offers engaging mobile games for exercise.

If you have some insights about the report, drop me a line!

Want to get a more detailed view of the CEE startup & VC ecosystem in Q3 2024?

Discover our monthly, quarterly, and yearly reports:

- VC Transactions in CEE in 1Q 2024

- VC Transactions in CEE in 2Q 2024

- Central and Eastern European Startups Report 2024

- New VC Funds Investing in Europe — 3Q 2024

- TOP CEE funding rounds closed in July

- TOP CEE funding rounds closed in August

- TOP CEE funding rounds closed in September

Disclaimer: This report features VC rounds that have been publicly disclosed before the publication date or were shared by our VC and startup community. Grants, debt funding, and transactions below €50,000 were not considered. Furthermore, while we value all startups operating in CEE, we focus on companies originating from the region, self-identifying as CEE companies, or having a significant presence of CEE founders.

Sources: Vestbee VC & startup community, startup press releases, open data from web & social media sources, PFR’s (Polish Development Fund) reports, DaaS platforms such as Crunchbase and Dealroom.