Key takeaways

- The second quarter of 2024 witnessed a boost in global startup funding, climbing to $79 billion — a 16% increase from the previous quarter and a 12% rise from the $71 billion invested in Q2 2023. While the last quarter marked one of the highest funding levels since Q1 2023, it doesn't necessarily indicate a full recovery of the venture market. Since 2023, funding has been inconsistent, fluctuating quarter by quarter due to a rise in large growth rounds for pre-IPO companies and investments in the AI sector. The most recent quarter continues this trend.

- In Q2, European startups secured nearly $16 billion in funding, marking a 31% increase from the previous quarter and a 17% rise year-over-year. Both early and late-stage investments grew, with late-stage funding seeing a strong boost.

- For the first time in a decade, Europe outpaced Asia in quarterly funding, with Asian startups facing challenges due to US-China tensions. The UK led European markets with $6.7 billion, followed by France with $2.9 billion, while Germany saw a decrease to $1.8 billion.

- AI was the top-funded industry, attracting $3.3 billion, followed by financial services at $3 billion, and sustainability at $2.5 billion, fueled by large investments in renewable energy.

- Similar to previous quarters, there's a palpable sense of anticipation in Central and Eastern Europe, with funding amounts reverting to levels seen in 2019-2020 and stakeholders eagerly awaiting a catalyst to reignite investor interest. While challenges persist, there's optimism for the future, and it's essential to remain vigilant and responsive to the evolving dynamics of the CEE region in the forthcoming quarters.

Global VC investment trends

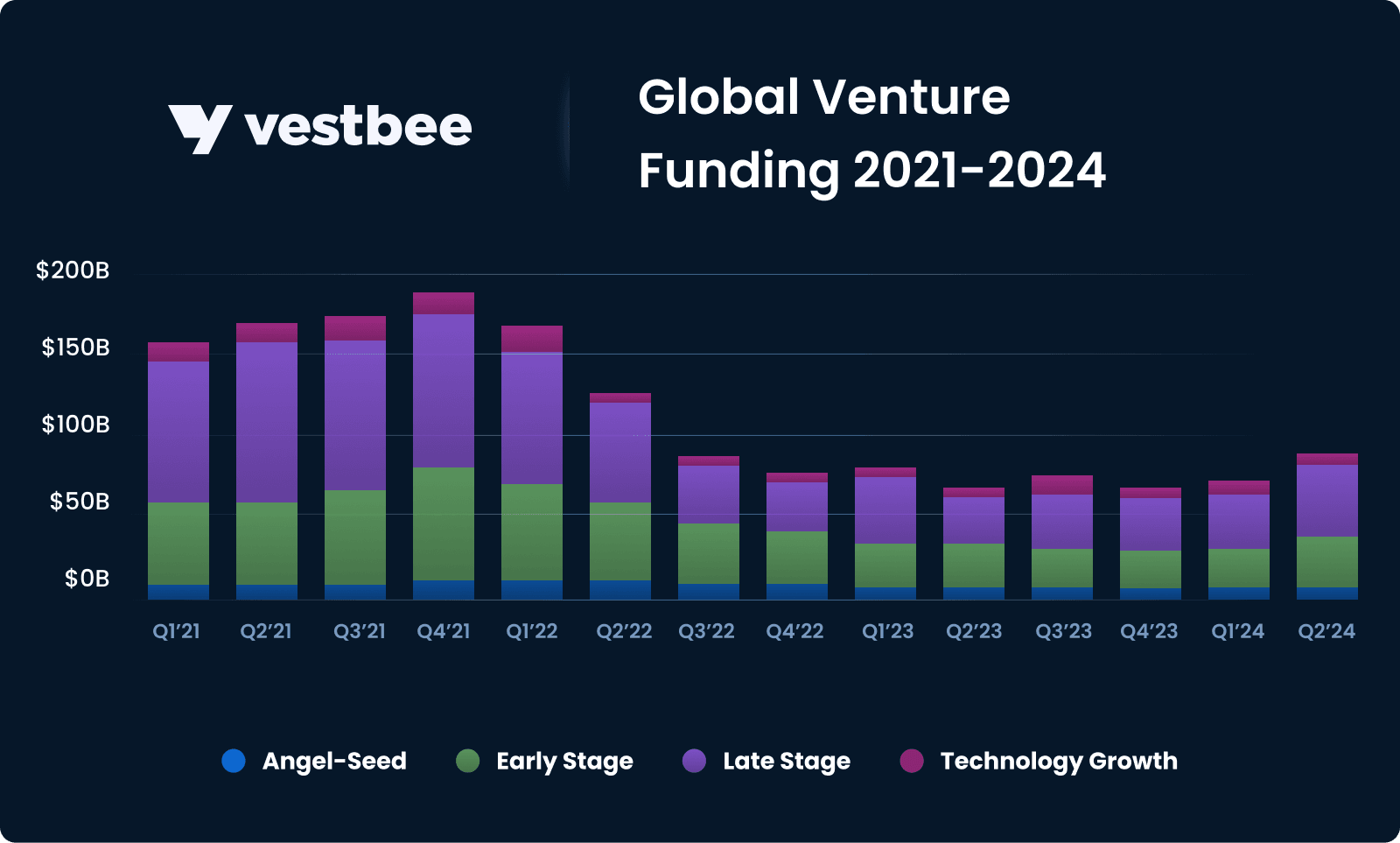

Global startup funding saw a boost in the second quarter, climbing to $79 billion — a 16% increase from the previous quarter and a 12% rise from the $71 billion invested in Q2 2023, according to Crunchbase. This growth was largely driven by mega-rounds, those $100 million and above, which significantly contributed to the overall increase.

Investment in AI companies more than doubled compared to the previous quarter, reaching $24 billion. This amount represents 30% of all venture dollars invested, making it the strongest quarter for AI funding in recent years. Additionally, there are indications that larger M&A deals gained momentum in Q2, offering much-needed liquidity to the venture capital market.

Crunchbase data shows that we are now eight to nine quarters into the current funding downturn. While the last quarter marked one of the highest funding levels since Q1 2023, it doesn't necessarily indicate a full recovery of the venture market. Since 2023, funding has been inconsistent, fluctuating quarter by quarter due to a rise in large growth rounds for pre-IPO companies and investments in the AI sector. The most recent quarter continues this trend.

Seed funding has been the most resilient during the downturn, maintaining stability over the last five quarters with approximately $8 billion invested per quarter. Although seed funding has decreased by about a third from its peak, it has held up better than early and late-stage funding in this slower investment climate. Analysis of Crunchbase data shows that companies are spending more time at the seed stage, as the criteria for raising Series A funding have become more stringent. This shift reflects the cautious approach investors are taking in the current market, making it more challenging for startups to progress to the next funding stage.

Late-stage funding saw a noticeable increase, reaching $36 billion in the second quarter of 2024, up from $33 billion in the same period last year. This growth was primarily driven by substantial investments in companies working on cutting-edge technologies such as AI foundation models, AI infrastructure, autonomous driving, and electric vehicles. Additionally, significant funding also flowed into sectors like cybersecurity, drug development, and quantum computing, reflecting investors' strong interest in these high-impact, future-oriented industries. This continued focus on late-stage rounds highlights the ongoing demand for mature companies that are advancing innovative solutions across multiple critical areas of technology.

VC investment trends in Europe

In Q2, funding for European startups saw a significant boost, reaching nearly $16 billion. This marks a 31% increase from the previous quarter and a 17% rise compared to the same period last year, according to Crunchbase data. Both early-stage and late-stage funding experienced growth, with a particularly strong uptick in late-stage investments.

Notably, for the first time in a decade, European startups attracted more quarterly funding than their counterparts in Asia. Asian startups, especially in China, faced their toughest quarter since late 2015, a situation exacerbated by ongoing US-China tensions.

Within Europe, the UK led the charge, securing $6.7 billion in funding, followed by France with $2.9 billion, both showing year-over-year growth. Germany, the third-largest market, saw a dip this quarter, with $1.8 billion invested in its startups.

AI emerged as the leading industry in Europe, attracting $3.3 billion in Q2. Major investments included London-based autonomous driving company Wayve, Paris-based Mistral AI, and Cologne’s language translation platform DeepL. The financial services sector followed closely, drawing $3 billion, with notable rounds raised by UK-based lending platforms Abound and GB Bank, as well as digital bank Monzo. Sustainability was the third-largest sector, with $2.5 billion invested, driven by significant mega-rounds in renewable energy companies, each exceeding $100 million.

Late-stage funding totaled $7.5 billion, spread across more than 100 rounds. While this represents a strong increase both quarter over quarter and year over year, it wasn’t the highest quarter we've seen in the past year, while early-stage funding reached $6.5 billion, distributed across just over 300 rounds. Notably, Series B funding at this stage saw the most significant year-over-year growth.

VC investment trends in CEE

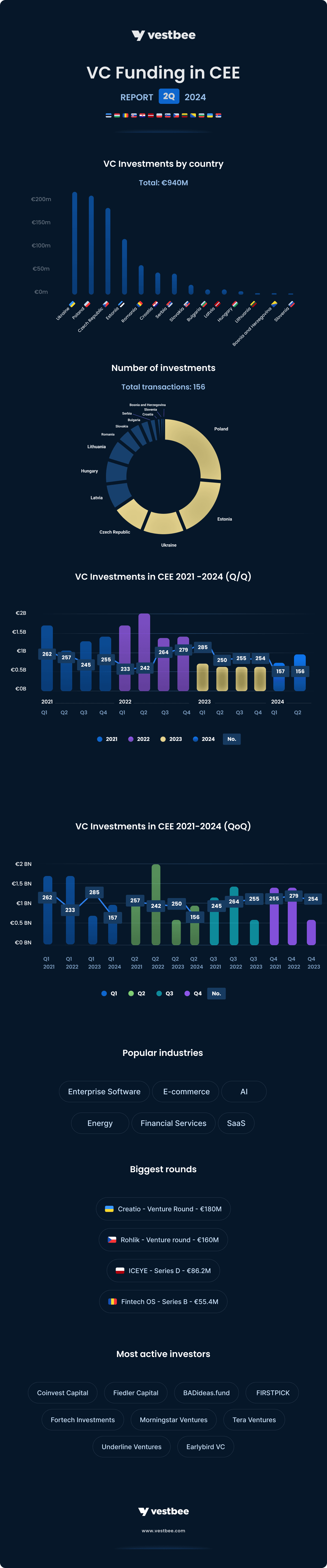

In Q2 2024, venture capital funding in the CEE region increased significantly to €940 million, up from €560 million in Q2 2023. However, this rise in capital was accompanied by a 35% drop in the number of funding rounds, from over 250 to just over 150.

This decline reflects ongoing challenges in securing investments due to tough economic conditions, reduced foreign fund activity, and a pause in public funding programs. Notably, nearly 70% of the total funding came from a few large rounds, underscoring the growing reliance on significant deals to drive overall market activity, while smaller rounds remain scarce.

Startup investment rounds in CEE in Q2 2024

- Number of funding rounds: 156 (136 fully disclosed in terms of amount, month, investors, and company details)

- The biggest disclosed investment rounds: Creatio, a €180M venture round, Rohlik, a €160M venture round, ICEYE, a €86.2M Series D round, Fintech OS, a €55.4M Series B round

- Total value of funding closed in CEE: over €940M*

- Countries with the highest number of funding rounds: Poland — 39 rounds, Estonia — 26, Ukraine — 18 rounds

- The most active VC funds: Coinvest Capital, Fiedler Capital, BADideas.fund, FIRSTPICK, Fortech Investments, Morningstar Ventures, Tera Ventures, Underline Ventures, Earlybird VC

- The most popular industries: Enterprise Software, E-commerce, AI, Energy, Financial Services, SaaS

*20 rounds undisclosed in terms of transaction value

Comparing Q2 2023 to Q2 2024, we see a mixed picture in the venture capital landscape. On the positive side, there’s been a significant increase in total funding value, rising from €560 million to €940 million. However, this growth in capital has been accompanied by a sharp decline of nearly 35% in the number of funding rounds, dropping from over 250 in Q2 2023 to just over 150 in Q2 2024. This decrease highlights the ongoing challenges companies face in securing investments, largely due to tougher economic conditions, a reduction in the activity of foreign funds in the CEE region, and a pause in public funding programs.

As in previous quarters, the market dynamics this quarter are heavily influenced by a few large funding rounds. These major rounds have raised nearly 70% of the total funding for the period. If we were to exclude these substantial investments, the overall picture of the market would look quite different. The reduced number of smaller funding rounds highlights a growing reliance on these significant investments to drive the total funding figures, indicating that the venture capital landscape remains uneven and concentrated around a few high-profile deals.

What shaped the CEE ecosystem in Q2 2024

In Q2 2024, a total of 156 venture capital transactions were recorded and the number of rounds each month remained stable throughout the quarter (47 in April, 48 in May, and 42 in June).

Some of the largest rounds disclosed in Q2 were secured by Ukrainian-founded (US-based) Creatio — €180M in a venture round, Czech Rohlik — €160M in a venture round, Polish (Finland-based) ICEYE — €86.2M in a Series D round, and Romanian (UK-based) Fintech OS — a €55.4M Series B round.

In the second quarter of 2024, Poland, Estonia, and Ukraine emerged as the most active countries, leading the region with 39, 26, and 18 funding rounds, respectively. These nations not only topped the list in terms of deal activity but also secured nearly 55% of the total funding for the quarter, reflecting their central role in the region's venture capital landscape. Czechia also stood out, contributing over 20% of the quarter's total funding, thanks in large part to Rohlik's substantial mega-round.

The investment trends during this period revealed a strong focus on key sectors such as Enterprise Software, e-commerce, AI, energy, financial services, and SaaS, indicating where investors see the most potential for growth and innovation in Central and Eastern Europe.

Now, let's discover the note-worthy and recently raised VC funds from CEE.

New VC funds from CEE in 2Q 2024:

- Bucharest-based venture capital firm Early Game Ventures has announced the launch of its €60 million Fund II, which will invest in early-stage startups across the CEE region.

- Warsaw-based Radix Ventures has announced the first €41 million close of a targeted €60 million deeptech fund. It aims to invest in 16–20 CEE startups.

- Ukrainian Venture Capital and Private Equity Association (UVCA) has launched a $300 million Fund of Funds to support the private equity, venture capital, and tech ecosystem in Ukraine.

- Prague-based venture capital firm Presto Ventures has launched a €150 million Presto Tech Horizons fund in collaboration with Czechoslovak Group (CSG). The fund will support security and defence tech startups from NATO countries.

- Hungarian and US-based Interactive Venture Partners launched €50 million inaugural fund, Interactive Venture Partners Fund LP, for pre-seed, seed, and Series A startups founded in CEE.

- Prague-based KAYA VC, which invests in early-stage startups, is raising its fifth €80 million fund to support Slovak, Polish, and Czech startups.

Interested in other new VC funds investing in CEE and Europe? Check out our article New VC Funds Investing in Europe — 2Q 2024.

Let's take a closer look at the Q2 results on a month-by-month basis. However, this review was solely based on fully disclosed rounds (name of startup, closing date, round’s size, participating investors).

Investment rounds in June

- Number of funding rounds: 42

- The biggest investment rounds: Creatio, a €180M venture round, Rohlik, a €160M venture round, InoBat, a €20M Series C round

- Total value of funding secured in CEE: over €456M

- Countries with the most funding rounds: Ukraine — 9, Estonia — 7.

- The most active VC funds: Earlybird VC, EBRD

- The most appreciated industries: AI, Energy, Analytics, E-commerce, SaaS.

In June, the CEE startup landscape saw the most significant activity of the quarter, securing 50% of the total funding in Q2 2024. Over €456 million was invested across 42 disclosed funding rounds. Ukraine and Estonia led in terms of the number of rounds, with 9 and 7, respectively, but it was Ukraine and Czechia that made the biggest impact on total funding value. This was primarily driven by two mega-rounds: €180 million raised by Ukrainian-founded (US-based) Creatio, which became Ukraine's next unicorn with a valuation of €1.2 billion, and €160 million raised by Czech Rohlik. Together, these rounds accounted for nearly 75% of June's total funding, underscoring that, without them, the overall ecosystem activity would have looked much less robust.

When comparing June 2024 to the same period in 2023, there's a noticeable 33% decline in the number of funding rounds. Excluding the two mega-rounds, the total amount of funding would also show a decrease, highlighting the reduced activity of VC investors in the CEE region.

The most popular sectors for investment were AI, energy, analytics, e-commerce, and SaaS. Among the most active investors were Earlybird VC and the EBRD. Sapphire Ventures, Horizon Capital, Volition Capital, and StepStone Group also played significant roles, particularly through their participation in Creatio’s record-breaking round.

Find out more: TOP CEE funding rounds closed in June.

Investment rounds in May

- Number of funding rounds: 48

- The biggest investment round: FintechOS, a €55.4M Series B round, Stargate Hydrogen, a €42M seed round, Fintech Farm, a €29.6M Series B round.

- Total value of funding secured this in CEE: over €173M

- Countries with most funding rounds: Estonia — 8, Poland — 7 rounds, Hungary — 7 rounds

- The most active VC funds: Coinvest Capital, BADideas.fund

- The most appreciated industries: energy, AI, healthcare

May was the most active month in Q2 in terms of the number of funding rounds, with 48 disclosed deals. However, it was also the slowest in terms of total funding secured by startups in CEE, totaling just over €170 million. Notable investments included the ones into companies like Romania-founded (UK-based) FintechOS, a €55.4 million Series B, Estonian Stargate Hydrogen, a€42M seed, and Ukrainian (UK-based) Fintech Farm, a€29.6M Series B.

Geographically, Estonia, Poland, and Hungary led in funding activity with 8, 7, and 7 rounds respectively. However, Romania stood out by securing the most investment, exceeding €55 million, largely due to the significant FintechOS Series B round.

In May, notable investors included Coinvest Capital and BADideas.fund, along with Cipio Partners, Molten Ventures, Earlybird Venture Capital, BlackRock, OTB Ventures, and GapMinder Venture Partners, who were key players in the largest round of April — FintechOS’ Series B. The main areas of focus were AI, energy, fintech, and healthcare.

In summary, while May was the slowest month of the quarter in terms of total funding secured, it mirrored the same period in 2023. This suggests a continued stagnation in the venture capital ecosystem, with monthly fluctuations driven largely by a few significant rounds.

Find out more: TOP CEE funding rounds closed in May.

Investment rounds in April

- Number of funding rounds: 47

- The biggest investment round: ICEYE, a €86.2M Series E round, Kontakt.io, a €42.8M Series C round, Mobi Banka, a €33M venture round.

- Total value of funding secured in CEE: over €282M

- Countries with the most funding rounds: Estonia — 11 rounds, Poland — 7 rounds.

- The most active VC fund: Fiedler Capital, FIRSTPICK, Morningstar Ventures, Reflex Capital, Startup Wise Guys, Tera Ventures

- The most appreciated industries: fintech, energy, AI, spacetech

In April, startups in Central and Eastern Europe raised over €282 million across 47 disclosed funding rounds. Estonia and Poland stood out as the most active ecosystems, leading both in the number of deals and total capital raised, with Estonia securing 11 rounds totaling €148 million and Poland closing 7 rounds with €40 million. Meanwhile, Croatia and Serbia made a significant impact, raising €27 million and €34 million respectively, highlighting their growing presence in the region's venture landscape.

Among notable funding rounds were the ones secured by Polish (Finland-based) ICEYE, a€86.2M Series D, Polish (US-based) Kontakt.io, a €42.8M Series C, and Serbian Mobi Banka, a€33M venture round. Investors maintained a strong interest in sectors such as AI, Fintech, Energy, Space and SaaS industries. Among the most active investors this month in the CEE landscape were Fiedler Capital, FIRSTPICK, Morningstar Ventures, Reflex Capital, Startup Wise Guys, and Tera Ventures. Solidium Oy, Move Capital, and Blackwells Capital are also worth distinguishing thanks to their participation in the biggest round this month — ICEYE’s series E.

In summary, venture funding in Central and Eastern Europe saw an increase compared to the same period in 2023. However, it's important to highlight that this growth was largely driven by a few major rounds. In fact, the three largest rounds in April accounted for nearly 60% of the total funds raised by startups that month.

Find out more: TOP CEE funding rounds closed in April.

Now let’s look closer at the top 50 funding rounds closed in CEE between April and June 2024.

Top 50 CEE startup funding rounds closed in Q2 2024:

- Rohlik is an online grocery platform that offers fast delivery and a wide product range.

- ICEYE is a defense and space company that delivers unmatched persistent monitoring capabilities for any location on Earth.

- Stargate Hydrogen is a Hydrogen tech firm that provides affordable green hydrogen to lower emissions in heavy industries.

- Mobi Banka is a Serbian mobile online bank, offering easy and convenient financial management via smartphone or computer.

- Fintech Farm, helps traditional banks create and run digital banks with a full tech stack and customer-focused solutions.

- Creatio develops a no-code CRM and workflow automation platforms, helping its customers digitize workflows and increase the productivity of commercial and operational teams.

- FintechOS is an end-to-end financial product management platform that Change the way you define, distribute, underwrite, service, and manage insurance and banking products

- Green Energy Park is establishing a global supply chain for green ammonia by building a major import and supply hub on the island of Krk in Croatia.

- InoBat develops and manufactures custom electric batteries for the automotive, commercial, motorsport, and aerospace sectors.

- Eldrive operates a major EV charging network in the SEE region, connecting and managing charging points through a smart platform for drivers, fleets, and locations.

- SmartLunch is a meal catering platform that manages and distributes group meals for companies, offering a convenient solution for employees.

- GA Drilling provides global drilling solutions for a carbon-free and energy-independent future using advanced geothermal technology.

- Quantum Innovations is a medtech startup focused on developing technology to improve safety in cardiac surgery, cardiology, and pulmonary medicine.

- CampusAI offers a platform called Blended Learning 3.0 for creating virtual worlds, attending classes, and customizing learning paths to enhance skills and organizational efficiency using AI.

- Entrio is an event management platform for in-person, hybrid, and virtual events, providing ticketing, promotion, cashless payment, and analytics solutions.

- Bisly is a smart building automation platform that develops hardware and software solutions to tackle scalability, cost, and integration challenges in smart buildings.

- Cookie3 is a blockchain startup specializing in behavioral analytics by interpreting customer profiles through wallet history.

- Euroloop is a calibration center for high-flow gas and liquid meters, ensuring precise measurement of oil and gas with customized testing and calibration.

- Portail.ai helps small to medium-sized businesses streamline operations by centralizing and analyzing data from various platforms to support decision-making.

- Gideon produces Visual AI-based mobile robots that enhance and automate operations, allowing humans and robots to collaborate more efficiently.

- Parkl Digital develops a mobile app for digital parking and EV charging services tailored for office buildings and companies.

- SensusQ is a defense tech startup offering software that integrates diverse data sources to provide actionable intelligence for military units.

- Spike is a data technology startup that helps healthcare and digital health companies integrate AI into their apps.

- Unmanned Dynamics develops advanced guidance systems for UAVs and uses these technologies to create hybrid cargo drones that can lift 50 kg and fly for 4-5 hours.

- E Money Network creates a modular blockchain that connects DeFi and real-world assets, linking Web 2.0 and Web 3.0 liquidity.

- Saltz is a fresh products marketplace that connects premium producers directly with customers from across 5 countries in Europe.

- Unnamed Defense Systems develops AI-driven swarm technology, integrating modern battlefield management systems with unmanned aerial vehicles (UAVs).

- Apify creates software for web scraping and automation, helping developers collect and manage data from websites.

- Deligo is a visual recognition software developer that uses AI and computer vision to quickly identify food and items, speeding up the checkout process and helping retailers assist their customers.

- Zeta Labs is a startup developing an AI assistant to automate routine web-based tasks.

- Raven is a high-frequency trading firm using advanced technology to execute fast trades and improve market efficiency.

- Proofs.io creates software that enables companies with APIs to quickly build AI-powered proof-of-concept apps tailored to their prospects' needs.

- AutoLayer develops an LRT app on Arbitrum, offering DeFi access to assets and liquidity, while focusing on deeper integration with the EigenLayer ecosystem.

- Behavio is a brand management solution offering a tracking and ad testing tool that delivers insights across 13 countries using advanced behavioral research.

- Delta Green is an energy tech company that creates solutions for flexible electricity use, renewable energy, and reduced power plant emissions.

- Supersimple develops a data search platform that allows SaaS teams to answer complex data questions in plain English without coding.

- SprayVision develops intelligent coating solutions for optimizing and controlling paint processes, including parameter settings and wet paint thickness measurement.

- ScoutLabs is an agritech startup that provides a digital trap network for monitoring insect migration and swarming, delivering data-driven, sustainable pest control solutions.

- Genezio is a type-safe serverless platform that offers tools for full-stack developers to build, deploy, test, and scale applications efficiently.

- Nanordica Medical is a health tech startup specializing in antibacterial nanoparticle technology that significantly enhances the treatment of infected wounds over traditional methods.

- 10Lines is a robotics startup that develops autonomous parking lot marking robots and technological tools to boost productivity in the sidewalk marking sector.

- ForActive develops an app that facilitates payment processing, communication, and community-building for independent sports service providers and their clients.

- SaleSqueze is a visual CPQ platform that streamlines complex product sales for small to medium-sized businesses across various industries.

- Collabwriting is a collaborative research platform with a Chrome extension for saving web snippets and an AI bot for finding research papers.

- CTO2B develops a platform that streamlines cloud service adoption and operations with automated DevOps solutions for various cloud platforms.

- heybooster is an AI-powered analytics platform that helps marketing teams identify revenue growth opportunities and fix budget inefficiencies by analyzing data from multiple channels.

- Native Teams is an all-in-one platform offering global work solutions for freelancers, remote workers, and their employers.

- Liledu offers a monthly subscription service delivering premium, personalized educational toys tailored to children's developmental stages from 6 months to 7 years.

- Zerops offers a platform that simplifies application development and management by automating infrastructure and scaling for solo developers and small teams

- Kontakt.io is a Journey Analytics Platform that uses AI, IoT, and RTLS to help businesses uncover waste, streamline capacity and improve workflows.

If you have some insights about the report, drop me a line!

Want to get a more detailed view of the CEE startup & VC ecosystem in Q2 2024?

Discover our monthly, quarterly, and yearly reports:

- VC Transactions in CEE in 1Q 2024

- Central and Eastern European Startups Report 2024

- New VC Funds Investing in Europe — 2Q 2024

- TOP CEE funding rounds closed in April

- TOP CEE funding rounds closed in May

- TOP CEE funding rounds closed in June

Disclaimer: This report features VC rounds that have been publicly disclosed before the publication date or were shared by our VC and startup community. Grants and transactions below €50,000 were not considered. Furthermore, while we value all startups operating in CEE, our focus is on companies that originate from the region, self-identify as CEE companies, or have a significant presence of CEE founders.

Sources: Vestbee VC & startup community, startup press releases, open data from web & social media sources, PFR’s (Polish Development Fund) reports, DaaS platforms such as Crunchbase and Dealroom.