VC landscape in Q3 2024

Crunchbase data shows that contrary to the previous upward trend, global venture funding declined in Q3 2024, reaching $66.5 billion — a 16% decrease quarter-over-quarter and a 15% decline year-over-year. This suggests a cooling in VC activity across sectors compared to Q2 2024.

AI continues to dominate, along with healthcare and biotech

In Q3 2024, AI led in venture funding, attracting nearly $19 billion or 28% of total investment, marking its second-highest quarter since ChatGPT's launch. Healthcare and biotech followed with over $15 billion, hardware raised $13 billion, and financial services garnered close to $8 billion.

VC trends to watch in coming quarters

According to the latest KPMG Venture Pulse report, VC investment and exit activity may remain soft in the fourth quarter, particularly until after the US election. However, optimism for a 2025 rebound is rising. M&A could lead the way as interest rate cuts attract deal interest.

AI will remain a top investment area, focusing on companies demonstrating tangible value, alongside increasing regulatory scrutiny for safety and privacy. Interest in alternative energy solutions, which has dipped recently, may surge next year as global energy demand is expected to surpass supply.

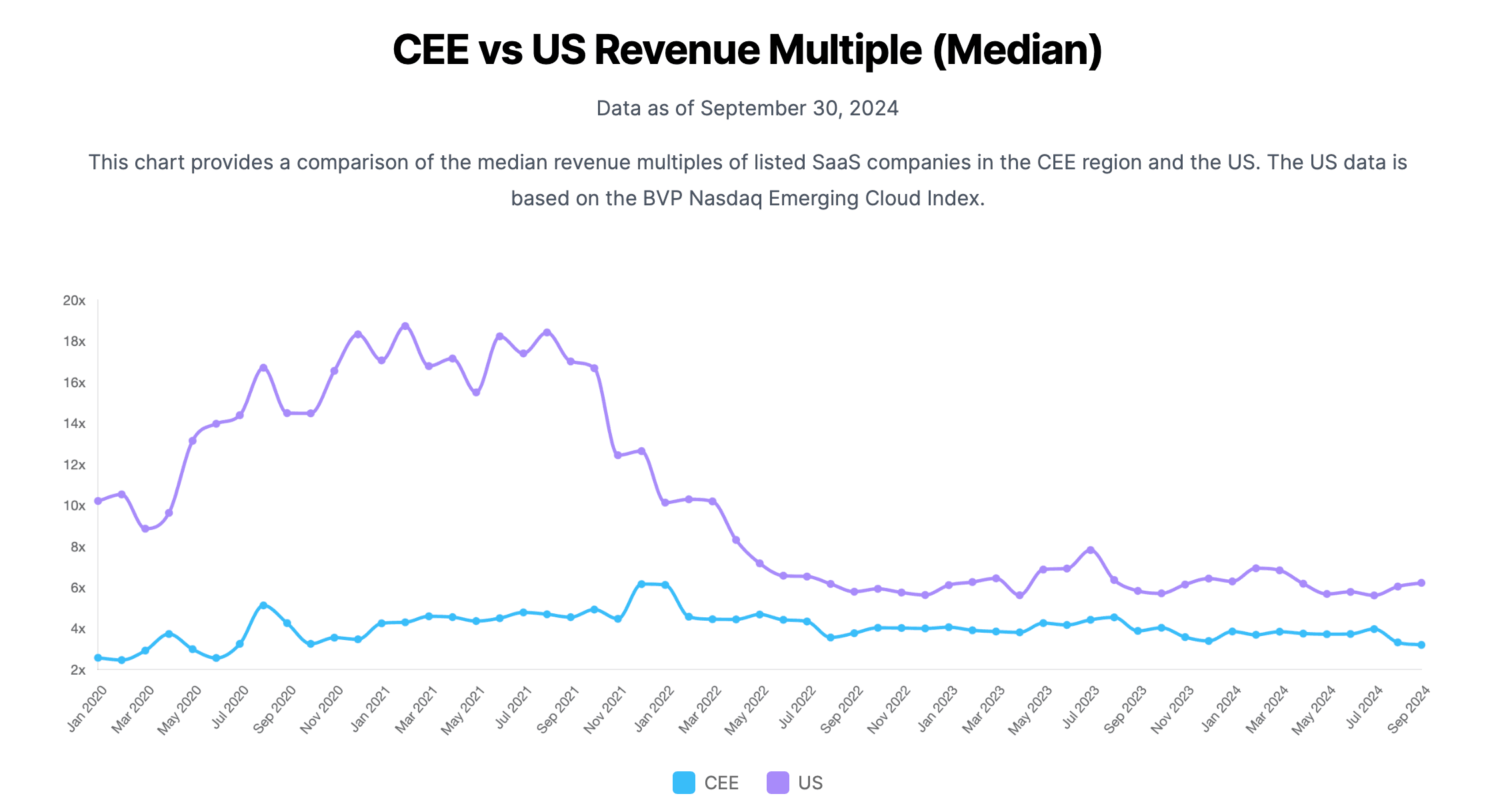

SaaS Companies in Q3 2024

Public SaaS companies have shown mixed performance, with the BVP Nasdaq Emerging Cloud Index revenue multiple amounting to 6,23x annualized revenue at the end of Q3 2024 — up 7,5% compared to the end of Q2 but, down 3% compared to 6,44x at the end of 2023, still demonstrating a cautious market sentiment.

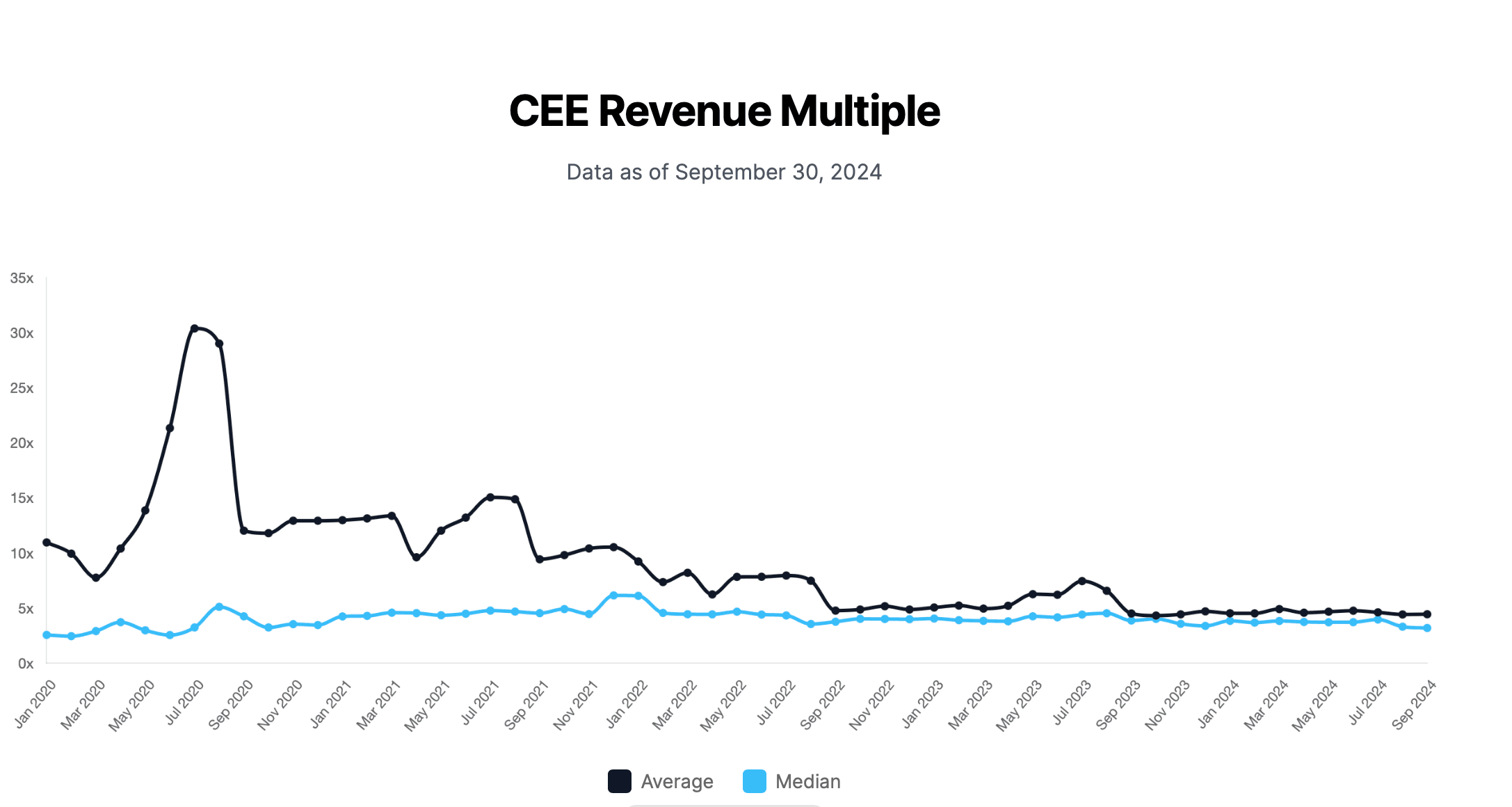

About CEE SaaS Index

CEE SaaS Index is a simple tool for startups and investors to value SaaS companies in Central & Eastern Europe based on revenue multiples from publicly traded SaaS companies from the CEE region, developed by Vestbee and Warsaw Equity Group.

While revenue multiples from publicly traded SaaS companies can provide a helpful starting point for valuation, currently available indexes are only based on US-listed SaaS companies, leaving the CEE region without relevant benchmarks, despite the region's thriving startup ecosystem and quadrupled VC funding over the last three years.

With projected growth and increased investment in CEE tech companies, a more appropriate valuation benchmark for regional startups and investors is required. To meet this need, Vestbee and the Warsaw Equity Group have collaborated to develop the CEE SaaS Index, providing a relevant benchmark for regional and international investors.

Key updates on Index performance for September 2024 include:

- The median CEE revenue multiple at the end of Q3 2024 decreased to 3,21x annualized revenues (3,74 at the end of Q2 2024) and decreased YoY (3,89 at the end of Q3 2023)

- The market capitalization of all companies included in the CEE SaaS Index remained stable at circa €2 billion as compared to the end of Q2 2024 and up 15% since the beginning of the year (€1.75 billion at the end of 2023).

- For comparison, the median US revenue multiple at the end of Q3 2024 amounted to 6,23x annualized revenue — down 3% compared to 6,44x at the end of 2023 and is 66% lower than its record high of 18,34x in December 2021.

- US multiples have seen a slower pace of decline than ones in the CEE over three quarters of 2024, and they are now 94% higher than CEE multiples (up from 90% at the end of 2023).

- CEE-based companies are growing slower than their US counterparts — 7,3% vs 15% YoY median revenue growth rate.