Key takeaways

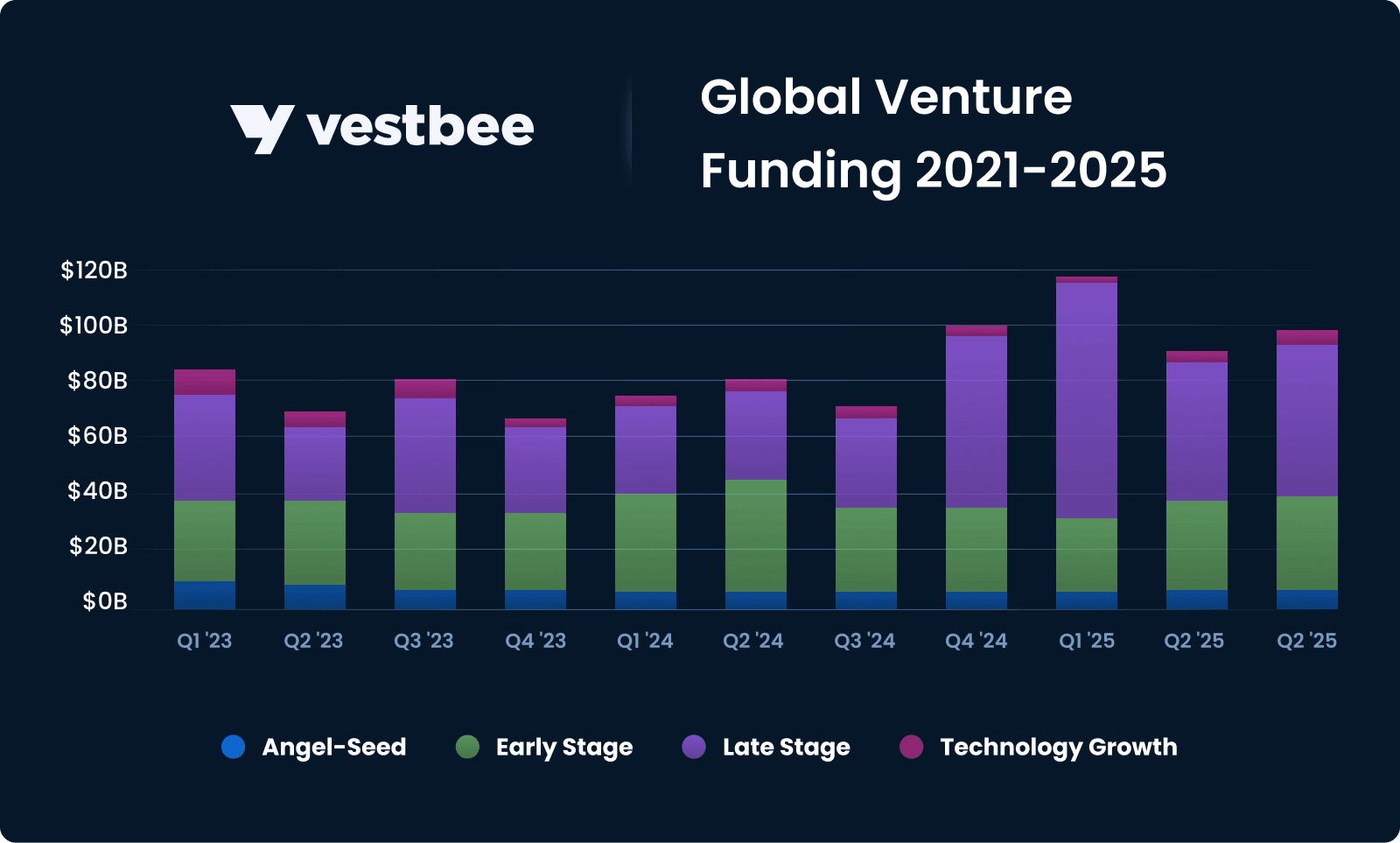

- Global venture funding rebounded in Q3 2025, reaching around $97 billion — a 38% year-over-year increase and the fourth consecutive quarter above $90 billion.

This growth was driven by a concentration of capital in megadeals, with 18 companies capturing a third of total investment, led by major AI rounds from Anthropic, xAI, and Mistral AI. Late-stage funding surged 66%, while early- and seed-stage funding remained stable, supporting a healthy pipeline of startups. The U.S. remained the dominant player, accounting for nearly two-thirds of global venture capital. IPO activity gained momentum, showcasing renewed investor confidence in large-scale tech innovation.

- European startups raised $13.1 billion across more than 1,000 deals in Q3 2025, reflecting a 22% year-over-year growth and stable quarterly performance.

Early-stage investments dominated, accounting for 60% of total funding, driven by strong interest in deep tech, biotech, and AI, with major rounds led by Paris-based Mistral AI and London’s Nscale. While growth-stage funding accounted for just 9% of global late-stage activity, seed funding remained robust at $1.7 billion. Although Europe trails the U.S. in later-stage capital, its vibrant early-stage ecosystem and sustained global investor engagement, underscored by four of the nine billion-dollar acquisitions worldwide originating from the region, show regional strengths. This steady foundation positions Europe to produce the next generation of globally competitive startups ready to scale internationally.

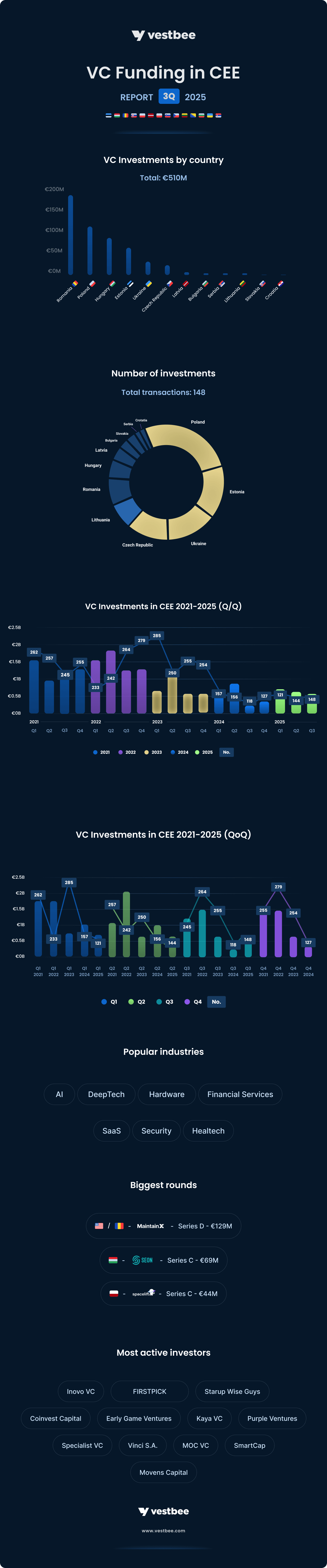

- Central and Eastern Europe’s startups raised over €510 million across 148 funding rounds in Q3 2025.

While a few large deals from MaintainX, Seon, and Spacelift accounted for a significant portion of the capital raised, most investment rounds were smaller, highlighting a cautious investor approach. Mirroring global trends, funding remains concentrated among select high-potential companies, with continued focus needed to broaden the investor base and build a resilient, scalable ecosystem.

Global VC in Q3 2025: AI funding explodes with multi-million rounds

Global venture funding made a strong comeback in Q3 2025, climbing 38% year over year to reach around $97B, according to Crunchbase. That’s up from 70 billion a year earlier and slightly higher than the 92 billion reported in Q2. For the fourth quarter in a row, total investment stayed above the 90 billion mark — a level last seen in 2022 —showing that investor appetite is slowly returning after two years of market correction.

Dominant sectors

What’s driving the rebound? Bigger bets on fewer players. Over 30 percent of all venture dollars in Q3 went into rounds of 500 million or more, with 18 companies alone capturing a third of global investment. The biggest checks went to headline-making AI players like Anthropic, which raised a staggering $13 billion, xAI, which raised $5.3 billion, and Mistral AI, which raised $2 billion. Other billion-plus deals went to Princeton Digital Group, Nscale, Cerebras Systems, Figure, Databricks, and PsiQuantum. The trend is clear — capital is concentrating in companies building the infrastructure and computing power underpinning the next wave of AI.

AI dominated Q3 funding overall, pulling in roughly $45 billion, or about 46 percent of total global venture investment. Nearly a third of that went to Anthropic alone. Hardware came in second, raising $16.2 billion across robotics, semiconductors, quantum computing, and data infrastructure startups. Healthcare and biotech raised $15.8 billion, while financial services raised $12 billion. The U.S. remained the epicenter of activity, accounting for nearly two-thirds of global venture funding, at about $60 billion.

Funding trends across stages

Late-stage deals saw the sharpest gains, rising more than 66 percent year over year to $58 billion. Early-stage funding also ticked up, totaling around 30 billion across 1,700 companies — a healthy sign that growth capital is still flowing beyond the biggest names. Seed activity held steady at roughly 9 billion across 3,500 young startups, continuing to feed the innovation pipeline despite capital concentration at the top.

Exits and IPOs

Meanwhile, IPO activity picked up pace for the second straight quarter. Sixteen venture-backed companies went public at valuations above $1 billion, collectively exceeding $90 billion in market value. Standouts like Chery Automobile, Figma, Klarna, and Netskope helped solidify the recovery narrative taking shape across late-stage and public markets.

After another blockbuster quarter — and with AI leading nearly half of all venture capital flow — 2025 is shaping up as a year of recalibrated optimism. Investors are still writing big checks, but they’re doing it selectively, backing category leaders with the capital and credibility to define the next phase of tech innovation.

VC in Europe: Europe’s early-stage strength offsets late-stage slowdown

European startups raised $13.1B across more than 1,000 deals last quarter, flat compared to Q2 but up 22 percent year over year, according to Crunchbase. Early-stage funding made up about 60 percent of that total, driven by strong momentum in deep tech, biotech, and AI applications. In contrast, North America saw a surge in $500 million-plus megadeals — mostly AI-related — capturing 68 percent of global funding and channeling two-thirds of that into later stages.

Funding geography and sectors

AI also remained one of Europe’s brightest spots, attracting roughly $5.2 billion — about 40% of total regional funding — up more than double from a year ago. The largest rounds went to Paris-based foundation model startup Mistral AI, which closed a massive $2 billion round, and London’s Nscale, a one-year-old data center and cloud player, which raised $1.1 billion and subsequently secured another $433 million from backers including Nvidia, Nokia, and Dell. Other notable AI raises came from Sweden’s Lovable, the UK's Xelix, and Swiss robotics platform Auterion.

Funding trends across stages

Growth-stage funding totaled around $5.4 billion across 75 deals, accounting for only 9% of global late-stage venture activity — a smaller slice than other regions. Notable deals included London-based device maker Nothing, Dutch design platform Framer, and Italy’s embedded security startup Exein.

The real strength of Europe’s ecosystem, however, remained at the early stages. Early-stage investment grew 31 percent year over year, reaching $6.1 billion across more than 250 deals. Top rounds went to Finland’s IQM Quantum Computers, Belgium’s Aerospacelab, and the UK's materials science startup CuspAI. Seed-stage funding reached $1.7 billion across 745 rounds, reflecting 18% of global seed allocation and solid activity across energy, AI, biotech, and robotics.

While Europe still lags behind the US in the growth stage, its early-stage resilience tells a different story. The region continues to produce a steady stream of well-funded innovators and attract global investors’ attention. Four of the nine billion-dollar acquisitions worldwide in Q3 originated from Europe — another sign that the continent’s startup ecosystem has matured. As more European founders enter the US market earlier and scale internationally, the question shifts from catching up to when the next European decacorn will emerge.

VC investment trends in CEE

Central and Eastern Europe: a calm quarter masking big rounds of reliance

In the third quarter of 2025, startups across Central and Eastern Europe completed 148 publicly reported funding rounds, collectively raising over €510 million. Monthly activity held relatively steady, ranging from 31 to 54 rounds, with a slight dip in August reflecting the traditional summer slowdown in Europe’s venture cycle. The distribution of capital tells an uneven story. Much like global trends, total funding remained heavily influenced by a handful of large transactions — the rounds closed by MaintainX, Seon, and Spacelift, which together accounted for a significant share of all capital committed in the region.

Beyond these headline rounds, investment sizes remained modest, with only ten deals exceeding 10 million euros. This pattern reflects a cautious investor mentality favoring established startup leaders over riskier, earlier-stage opportunities. Market participants note this selectivity stems from both macroeconomic pressures and more strategic capital allocation to companies demonstrating clear scaling potential.

This dynamic presents a nuanced snapshot of the CEE venture landscape. While steady deal flow highlights ecosystem resilience and deepening entrepreneurial strength, the reliance on large, late-stage deals exposes vulnerability at the foundational level. Without enhanced early-stage capital availability and a wider base of engaged investors, both local and international, there is a real risk that innovation pipelines could narrow, jeopardizing the region’s future growth prospects.

However, this phenomenon is not unique to CEE. Globally, a third of venture funding in Q3 was concentrated among just 18 companies. This selectivity reflects a broader market preference for proven category leaders amid economic uncertainty, suggesting that CEE’s experience mirrors global shifts rather than regional failures.

Looking ahead, ecosystem stakeholders should emphasize the importance of broadening the investor base and encouraging more balanced capital deployment across all stages. Initiatives to stimulate earlier-stage funding, deepen local fund capabilities, and attract new cross-border investors are viewed as critical to sustaining momentum. While headline deals provide validation and visibility, long-term success will depend on nurturing a vibrant, inclusive entrepreneurial ecosystem that supports innovation from seed to growth.

In sum, the third quarter’s data offers a roadmap: CEE has demonstrated it can produce world-class startups, yet the challenge now lies in translating those successes into a durable and scalable venture ecosystem that can weather cycles and consistently deliver impact.

Startup investment rounds in CEE in Q3 2025

- Number of funding rounds: 148 (131 fully disclosed in terms of date and funding amount).

- The biggest disclosed investment rounds: MaintainX, a €129M Series D round, Seon, a €69M Series C round, Spacelift, €44M Series C round

- Total value of funding closed in CEE: over €510M* (total value includes Romanian-rooted but US-based MaintainX)

- Countries with the highest number of funding rounds: Poland — 39 rounds, Estonia — 25, Ukraine — 24 rounds

- The most active VC funds: Inovo VC, FIRSTPICK, Startup Wise Guys, Coinvest Capital, Kaya VC, Purple Ventures, Vinci S.A., Specialist VC, MOC VC, SmartCap, Movens Capital, Early Game Ventures

- The most popular industries: AI, DeepTech, Hardware, Financial Services, SaaS, Security, and Healtech.

*17 rounds undisclosed in terms of transaction value.

What shaped the CEE ecosystem in Q2 2025

Central and Eastern Europe’s venture capital market held steady through the second quarter of 2025, recording 148 funding rounds across the region. Activity was evenly distributed, with 46 disclosed investments in July, 31 in August, and 54 in September. The slight dip in activity during July is likely due to the traditional summer slowdown that affects much of Europe’s venture ecosystem, with many funds and founders pausing fundraising efforts during the holiday months.

A handful of standout transactions accounted for the bulk of the capital inflow. Romanian-rooted, US-based MaintainX closed a €129 million Series D round, setting a record for the region this quarter. Hungary’s Seon followed with a €69 million Series C, while Poland’s Spacelif secured €44 million in its Series C. On the one hand, these larger rounds lifted the region’s quarterly totals and underscored how CEE-born companies are increasingly scaling across borders and attracting international venture capital. Without the MaintainX round, however, the region’s overall funding volume would paint a more tempered picture, highlighting how a few standout deals continue to heavily influence aggregate statistics in the CEE venture landscape.

On the country level, Poland, Estonia, and Ukraine remained the most active ecosystems, recording 39, 25, and 24 deals, respectively. Together, they contributed to nearly 60% of all transactions and around 40% of total capital raised. This persistent concentration of activity highlights the dominance of established startup hubs and the growing role of regional investors increasingly doubling down on familiar markets. Romania, however, emerged as the funding leader in Q2, surpassing €186 million, thanks largely to MaintainX’s mega round.

Sectorally, investor focus in CEE mirrored broader European and global trends, with most activity flowing into AI, deep tech, hardware, fintech, SaaS, cybersecurity, and healthtech. The growing participation in frontier and infrastructure technologies highlights CEE’s evolution from an outsourcing hub toward a serious innovation engine, particularly in technical verticals.

Let’s note that while deal volumes remain relatively stable, the quality of rounds — particularly in terms of investor mix and valuation confidence — continues to improve. The region is seeing a maturing founder base, increased interest from Western European and US funds, and a higher incidence of serial entrepreneurs reinvesting domestically. If this trend persists, CEE could transition from being viewed as a value market to a region producing globally competitive startups on its own terms.

Now, let's discover the noteworthy and recently raised VC funds from CEE.

New VC funds from CEE in 3Q 2025:

- Czech Aspire11 has launched its inaugural €500 million pension-backed fund.

- Ukrainian Flyer One Ventures has raised a €50 million Fund V to invest in early-stage tech companies in Ukraine and the CEE.

- vastpoint, a new VC firm set up to back Polish tech talent, has raised $22 million for its debut fund.

- Riga- and Stockholm-based venture capital firm Outlast Fund has announced the closing of its first fund at €21 million to invest in pre-seed and seed-stage startups across the Baltic and Nordic regions.

- Darkstar has made the first €15 million close of its pan-European defence fund.

- Ukrainian VC fund D3 has raised $5 million to invest in defence tech innovation, including drones, sensors, demining tools, and AI solutions, in Ukraine and Europe.

Interested in other new VC funds investing in CEE and Europe? Check out our article New VC Funds Investing in Europe — 3Q 2025.

Let's take a closer look at the Q3 results on a month-by-month basis. However, this review was based solely on fully disclosed rounds (the startup's name, the closing date, the round size, and the participating investors).

Investment rounds in September

- Number of funding rounds: 54

- The biggest investment rounds: Seon, a €69M Series C round, DRUID AI, €26.8M Series C, xMoney, €18.6M venture round

- Total value of funding secured in CEE: over €188M

- Countries with the most funding rounds: Poland — 10, Ukraine — 10, Lithuania — 9

- The most active VC funds: Kaya VC, Purple Ventures, Movens Capital, Early Game Ventures

The most appreciated industries: AI, Security, Healthtech

In September 2025, startups across Central and Eastern Europe raised over €188 million through 54 disclosed funding rounds. Poland, Ukraine, and Lithuania led in the number of transactions, with 10, 10, and 9 deals, respectively, while Hungary and Romania topped the charts in capital raised. The standout rounds for Seon and DRUID AI were the key drivers behind this surge, setting the pace for the month’s funding dynamics.

Combined, these two transactions accounted for more than half of all capital deployed in September, further underlining how a few large-scale deals continue to shape the region’s aggregate numbers. Without these high-value rounds, the underlying investment volume would appear considerably more restrained, reflecting the ongoing challenge of limited depth in later-stage capital.

Sectoral activity was concentrated in technology-driven verticals such as AI, cybersecurity, and healthcare. Local funds, including Kaya VC, Purple Ventures, Movens Capital, and Early Game Ventures, remained actively engaged across numerous deals, while continued participation from international investors like Hoxton Ventures and Institutional Venture Partners reaffirmed cross-border confidence in the region’s most promising technology companies.

Find out more: Top CEE funding rounds closed in September.

Investment rounds in August

- Number of funding rounds: 31

- The biggest investment round: Bisly, a €4.3M venture round, Handwave, a €3.6M Seed

- Total value of funding secured this in CEE: over €25M

- Countries with the most funding rounds: Ukraine — 8, Estonia — 7 rounds

- The most active VC funds: FIRSTPICK

- The most appreciated industries: AI, SaaS, Healthtech, Fintech

August 2025 emerged as the quietest month for venture activity in Central and Eastern Europe during the third quarter, with startups collectively raising just over 25 million euros through publicly disclosed rounds. The month’s largest deal was Bisly’s 4.3 million-euro financing, while most transactions fell within the early- and seed-stage range, reflecting an overall pause in larger rounds.

Ukraine and Estonia led by deal count, closing 8 and 7 transactions, respectively, pointing to the resilience of early-stage ecosystems in these markets even amid a broader funding lull. The relatively modest capital flow underscores the region’s dependence on timing and seasonality, as August typically sees a noticeable slowdown in European VC activity. In many countries, fund operations effectively pause for the summer break, causing deal processes and announcements to shift toward late Q3 or early Q4.

From an investor perspective, FIRSTPICK stood out as one of the most active venture firms in the region during the month, maintaining a steady investment pace despite the quieter environment. Sectoral allocation mirrored quarterly trends, with AI, SaaS, healthtech, and fintech continuing to attract the majority of available capital.

Slower months like August often serve as a time for funds to focus on portfolio management, pipeline evaluation, and planning for deal closures in September and October, when activity historically rebounds.

Find out more: Top CEE funding rounds closed in August.

Investment rounds in July

- Number of funding rounds: 46

- The biggest investment round: MaintainX, a €129M Series D round, Spacelift, €44M Series C round, Lightyear, a €19.9M Series B

- Total value of funding secured in CEE: over €260M

- Countries with the most funding rounds: Estonia —11 rounds, Poland — 9 rounds

- The most active VC fund: Bessemer Venture Partners, Bain Capital Ventures, due to participating in the biggest investment round this month/quarter

- The most appreciated industries: Enterprise Software, Fintech, AI, and Health.

In July 2025, startups across Central and Eastern Europe collectively raised more than 260 million euros through 46 publicly disclosed funding rounds. While the month featured a few headline-grabbing transactions, the broader funding landscape remained restrained, with capital flows concentrated around a small number of established scale-ups. The standout round by MaintainX once again influenced aggregate numbers upward — if isolated, the underlying pace of investment reveals a more moderate level of market activity and capital availability across the region.

Estonia and Poland emerged as the most active ecosystems, closing 11 and 9 deals, respectively. Activity remained focused in familiar verticals such as enterprise software, fintech, artificial intelligence, and health technology - sectors that continue to attract steady investor attention both regionally and across Europe.

Among investor activity, global venture firms such as Bessemer Venture Partners and Bain Capital Ventures stood out for their participation in the quarter’s largest transaction — MaintainX’s €129 million Series D round — underscoring continued international confidence in select CEE-born, globally scaling startups.

Find out more: TOP CEE funding rounds closed in July.

Now, let’s look closely at the 50 most interesting CEE startups that closed rounds between July and September 2025.

Top 50 CEE startups that closed funding rounds in Q3 2025:

- Lightyear is a digital investing platform that provides access to global equity markets, money market funds, and multi-currency savings.

- Sympower.net is an energy flexibility provider, using AI-driven demand response and renewable energy solutions to help industrial businesses and battery owners monetize and optimize their energy consumption.

- Vok Bikes offers automotive-grade electric cargo bikes designed for heavy-duty urban deliveries

- Bisly is a cleantech startup specializing in AI-powered smart building automation systems that optimize energy use and indoor climate in residential and commercial buildings.

- Vocal Image is an AI platform for improving voice and speech.

- BetterPic specializes in AI-powered photography solutions for both individuals and enterprises.

- Jälle Technologies develops recycling technologies that extract valuable metals from used lithium-ion batteries and convert waste graphite into graphene-like materials.

- Better Medicine develops AI-powered tools for the early detection of kidney cancer. Its CE-certified platform analyzes medical imaging for faster, more accurate diagnosis.

- Creem is a fintech startup providing financial solutions for AI-native businesses.

- Handwave provides a secure, contactless palm-scan system for payments, ID verification, and loyalty rewards.

- Cellbox Labs creates automated organ-on-chip systems for animal-free drug testing.

- Tournated is an all-in-one sports management software that empowers sports organizations to create and manage their own platforms seamlessly.

- MELP is an employee well-being and engagement platform that helps organisations connect with their workforce through personalised benefits, recognition, and internal communication tools.

- Kashimi develops alternative payment infrastructure for regulated and licensed financial institutions.

- GREI is an AI-driven platform that integrates with existing cameras and sensors at large physical sites to provide real-time monitoring of operations, identify risks, and highlight inefficiencies.

- E2B provides a secure, open-source cloud platform for running AI-generated code and agentic workflows at scale.

- Talentiqa automates candidate pre-screening to streamline and accelerate hiring.

- TRIFFT is a SaaS platform that enables mid-sized brands to design and launch data-driven customer loyalty programs without requiring in-house technical resources.

- Supernova builds software for product teams to connect design systems, code, and product documentation in one platform.

- Spacelift is a DevOps automation platform that allows teams to manage infrastructure as code with streamlined cloud workflows.

- SR Robotics develops robotics solutions, including modular submarines for underwater operations and innovative cleaning robots for maritime and industrial applications.

- Eterny develops a platform to consolidate and manage personal financial and legal information.

- SEON is a fraud prevention and AML compliance platform that leverages over 900 first-party data signals and AI-driven analytics to help companies detect and prevent sophisticated fraud.

- Heatventors specializes in advanced thermal energy storage solutions, utilizing phase change materials to efficiently store and release heat or cold.

- DATAPAO is a Data Engineering and Data Science consulting firm covering the entire data journey.

- Proteine Resources produces premium insect-based protein and bioactive compounds for use in animal feed, veterinary supplements, cosmetics, and medicines.

- Fluence Technology is a developer and manufacturer of cutting-edge fiber-based femtosecond lasers for industrial, medical, and scientific applications.

- sun.store is a B2B marketplace for solar and energy storage equipment.

- Doctor.One enables healthcare professionals to stay continuously connected with patients between hospital or clinic visits through asynchronous communication, extending trusted doctor-patient relationships without overloading physicians' schedules.

- Beespeaker an edtech language learning app using AI and video lessons.

- SOLO Workout transforms traditional gym equipment into smart, connected machines through patented retrofit sensors, delivering real-time workout tracking, AI-powered coaching, and personalized training plans.

- Orbital Matter develops 3D printing solutions for in-space manufacturing.

- AIStats creates advanced metrics and event data using machine learning and computer vision to help football fans and clubs make better tactical and strategic decisions.

- Paymove fintech startup enabling QR code payments.

- ICEYE provides high-resolution radar satellite imagery for Earth observation.

- SI Robotics builds scalable humanoid robots designed to replace low-skilled labor in industrial and defense environments.

- Microamp builds portable, end-to-end 5G mmWave solutions for commercial, industrial, and defence applications.

- Trasti is building a fully digital insurance platform that distributes and underwrites motor insurance products from Triglav.

- MaintainX helps industrial teams manage work orders, asset performance, parts, and labor with AI-driven insights.

- DRUID AI automates business workflows with AI-powered applications.

- xMoney enables online businesses to accept payments via a wide range of instruments directly on their websites or platforms.

- LYS Protocol is a decentralized yield trading protocol offering efficient liquidity pools and auto-rebalancing strategies for defi investors.

- Meetgeek develops AI-driven tools that actively participate in meetings and calls, turning conversations into structured data, actionable tasks, and automated workflows.

- Paypercut develops a Buy Now, Pay Later (BNPL) aggregator platform that simplifies payment options.

- Blue Longevity Clinics is building a network of longevity centers in Southeast Europe, offering diagnostics, behavioral tools, and therapies like cryotherapy.

- Swarmer develops hardware-agnostic AI software that allows unmanned vehicles to act autonomously and operate in coordinated swarms.

- Liki24 connects consumers across Europe with pharmacies, drugstores, and health product suppliers through a centralized online platform.

- Clearly develops an AI-driven mental health platform that combines video sessions with licensed therapists, 24/7 AI companions, and standalone AI therapy.

- YOX develops an AI-powered job marketplace that matches blue-collar workers with employers.

- NORDA Dynamics develops autonomous drone control systems capable of operating without GPS or traditional communication channels and functioning under electronic warfare conditions.

If you have some insights about the report, drop me a line!

Want to get a more detailed view of the CEE startup & VC ecosystem in Q3 2025? Discover our monthly, quarterly, and yearly reports:

- VC Funding in CEE in 3Q 2024

- Central and Eastern European Startups Report 2025

- New VC Funds Investing in Europe — 3Q 2025

- TOP CEE funding rounds closed in July

- Top CEE funding rounds closed in August

- Top CEE funding rounds closed in September

Disclaimer: This report features VC rounds that have been publicly disclosed before the publication date or were shared by our VC and startup community. Grants, debt funding, and transactions below €50,000 were not considered. Furthermore, while we value all startups operating in CEE, our focus is on companies that originate from the region, self-identify as CEE companies, or have a significant presence of CEE founders.

Sources: Vestbee VC & startup community, startup press releases, open data from web & social media sources, PFR’s (Polish Development Fund) reports, DaaS platforms such as Crunchbase and Dealroom.